Are We About to See A Major Shift in the US Dollar? What it Means for the US Stock Market:

Systematic funds are aggressively selling global equities - are they worried about the dollar?

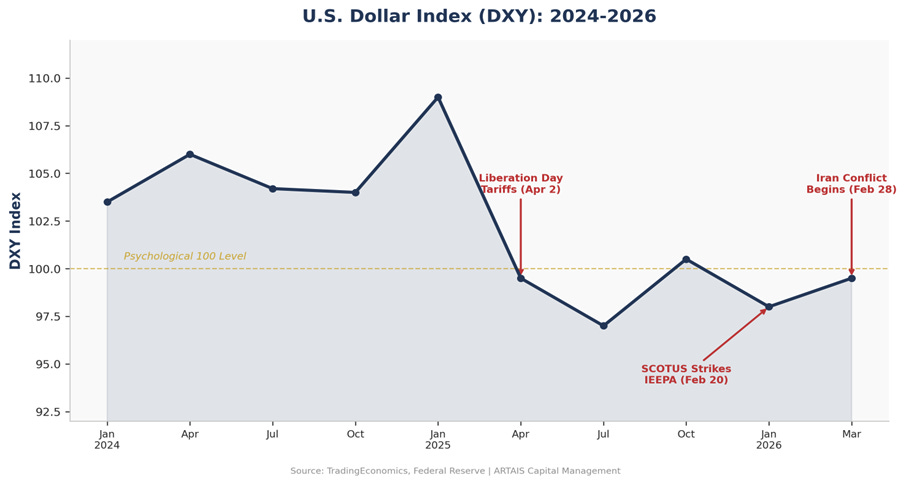

Yesterday, on X/Twitter, I was discussing the rising strength of the US dollar. I posted this chart showing how the dollar (using DXY as a proxy for the dollar) keeps hitting overhead resistance and has continuously failed to breakout since Trump took office for the second time.

With charts like this, I like to look at not just the level, but the catalysts that may cause the dollar to breakout or fail to breakout again.

Adam over at the Kobeissi Letter posted this chart from Goldman Sachs. The chart shows how systematic funds are starting to aggressively sell their global equity positions.

Why does this matter? Well, it is a potential signal that money managers are starting to take the viewpoint that the US dollar is about to get stronger.

Fellow Terp and CMT, Finnian Devine then shared this chart with me:

What May Cause the Dollar to Rise?

The big question is, what are these money managers worried about?

It’s inflation. It's still here. It’s still sticky.

As inflation continues to be a problem, the chances of further rate cuts from the Fed are starting to fade.

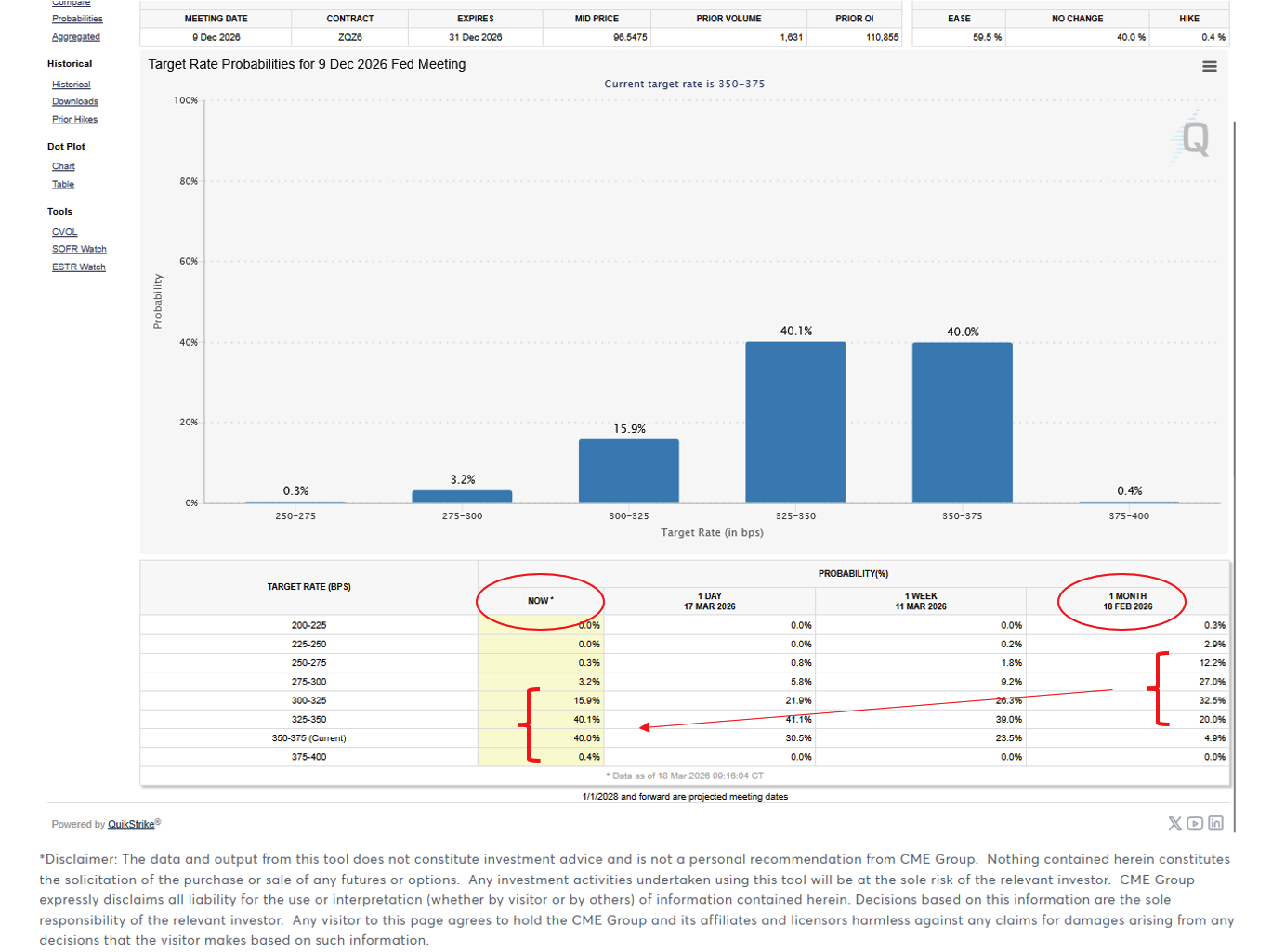

Below is the FedWatch Tool. It shows how the futures market is pricing the chances of future cuts/hikes by the Fed by the end of 2026:

Notice the shift in consensus from just a month ago. The odds of rates staying where they are have jumped from 4.9% to 40%.

The market is now indicating that we may get one or zero rate cuts for the rest of the year.

This will attract foreign capital.

Foreign Capital

The combination of higher US interest rates, a strengthening currency, and deep liquid capital markets creates a powerful pull for global savings. The higher inflow from overseas causes an increase in demand for the dollar. Thus, the dollar rises.

Foreign holdings of US assets exceed $35 trillion, with European investors alone holding approximately $8 trillion in US bonds and equities (Morgan Stanley data).

This capital attraction is self-reinforcing: foreign demand for dollar-denominated assets pushes the dollar higher, which increases returns for foreign investors, which attracts more capital.

The Consumer Benefits from a Strong Dollar

If the dollar does breakout and begin to strengthen, there will be a major benefit to consumers in the form of deflation.

A strong dollar makes imports cheaper, acting as a disinflationary force.

American consumers benefit from lower prices on imported goods such as electronics, automobiles, clothing, and energy.

In addition, most global commodities are priced in US dollars; when the US dollar is weaker, it increases their price for American buyers while making them cheaper for foreign purchasers (boosting demand). This adds to inflation.

Why Would We Not Want a Strong Dollar?

A strong dollar will have a negative impact on exporters. US goods become more expensive abroad, reducing competitiveness.

During the dollar’s 2010-2024 bull cycle (approximately 40% cumulative appreciation), US manufacturers consistently cited currency headwinds as a drag on international sales. The trade deficit widened substantially during this period, reaching record levels.

For example, when the dollar weakens 10%, a $100 American product effectively drops to $90 for a European buyer (assuming EUR/USD appreciation).

This price advantage accumulates across billions of dollars in annual trade flows. US sectors like manufacturing, agriculture, and technology services — sectors with significant export exposure — stand to benefit most directly when the dollar is weak.

Foreign consumers (they get lower prices) and US companies (they sell more overseas because they can underprice foreign competitors) are the clear winners when the dollar is weaker:

● EUR/USD: US goods became 11.8% cheaper for European buyers in 2025 (dollar fell 11.8% vs. the euro)

● USD/MXN: US goods became 13.5% cheaper for Mexican buyers (dollar fell 13.5% vs. the peso)

● GBP/USD: US goods became 7.5% cheaper for British buyers (dollar fell 7.5% vs. the pound)

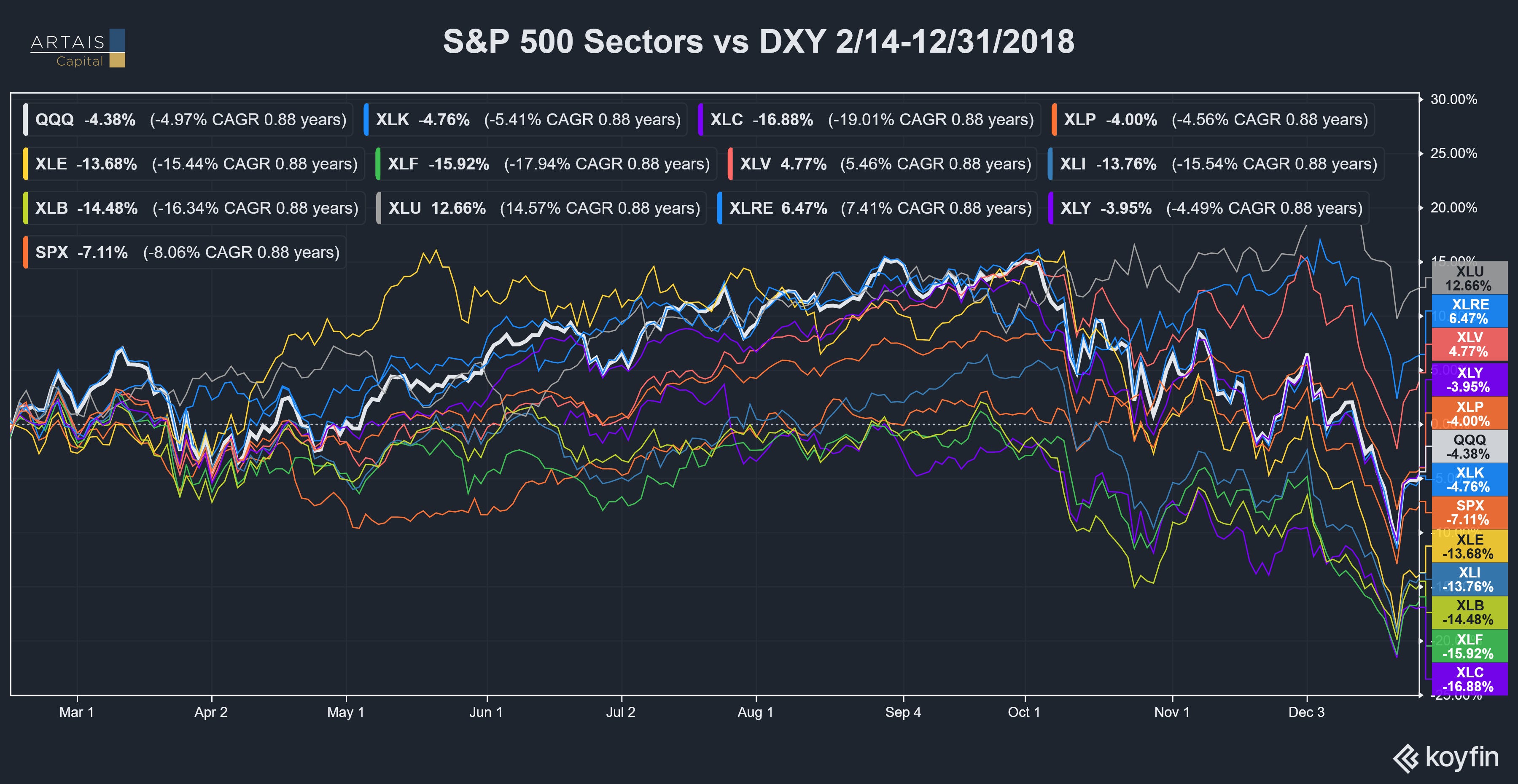

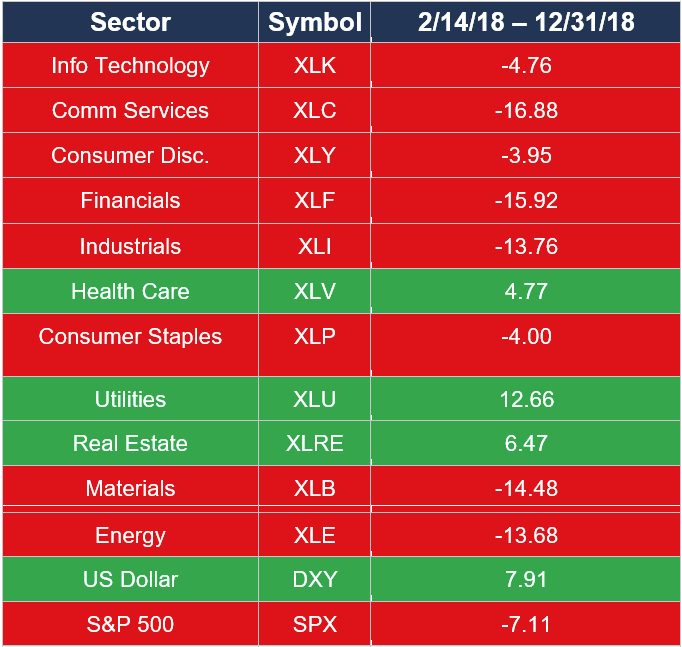

Looking Back at 2018’s Winners and Losers

While global political events can have a big impact on the market, I did want to look at the areas that did well during the rising dollar event that occurred in 2018.

Healthcare, Utilities, and Real Estate rose along with the dollar during this time, while the rest of the sectors and the S&P 500 declined:

Note: Past performance is not indicative of future results. Source: Koyfin

Every market cycle is different. Keep a close eye on the charts if/when the dollar starts to strengthen to see if similar patterns emerge, indicating we may see a repeat of 2018.

What I’m Watching

In addition to policy changes from the White House and the Fed, the charts tell the real story.

I want to see how the markets react at current levels. Do investors feel that there is value and an opportunity to invest in dollars at current levels?

Or do they feel that policies will be revised to push the dollar lower when/if the dollar begins to break out to the upside?

For now, I am paying close attention to DXY. A meaningful breakout above 100 is a notable move and may force changes to Wall Street’s outlook and US economic policies.

John Rothe, CMT

ARTAIS Capital Management

john.rothe@artaiscapital.com

Disclaimer

ARTAIS Capital Management, LLC (“ARTAIS Capital”) is a registered investment advisor offering advisory services in registered states and in other jurisdictions where exempt. Registration does not imply a certain level of skill or training.

The information on this site is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This information should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal any performance noted on this site.

The information on this site is provided “AS IS” and without warranties of any kind, either express or implied. To the fullest extent permissible pursuant to applicable laws, ARTAIS Capital Management, LLC disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.