Fewer and Fewer Stocks Are Holding This Market Up

Stocks are starting to run out of momentum, as history says it's time for a pause.

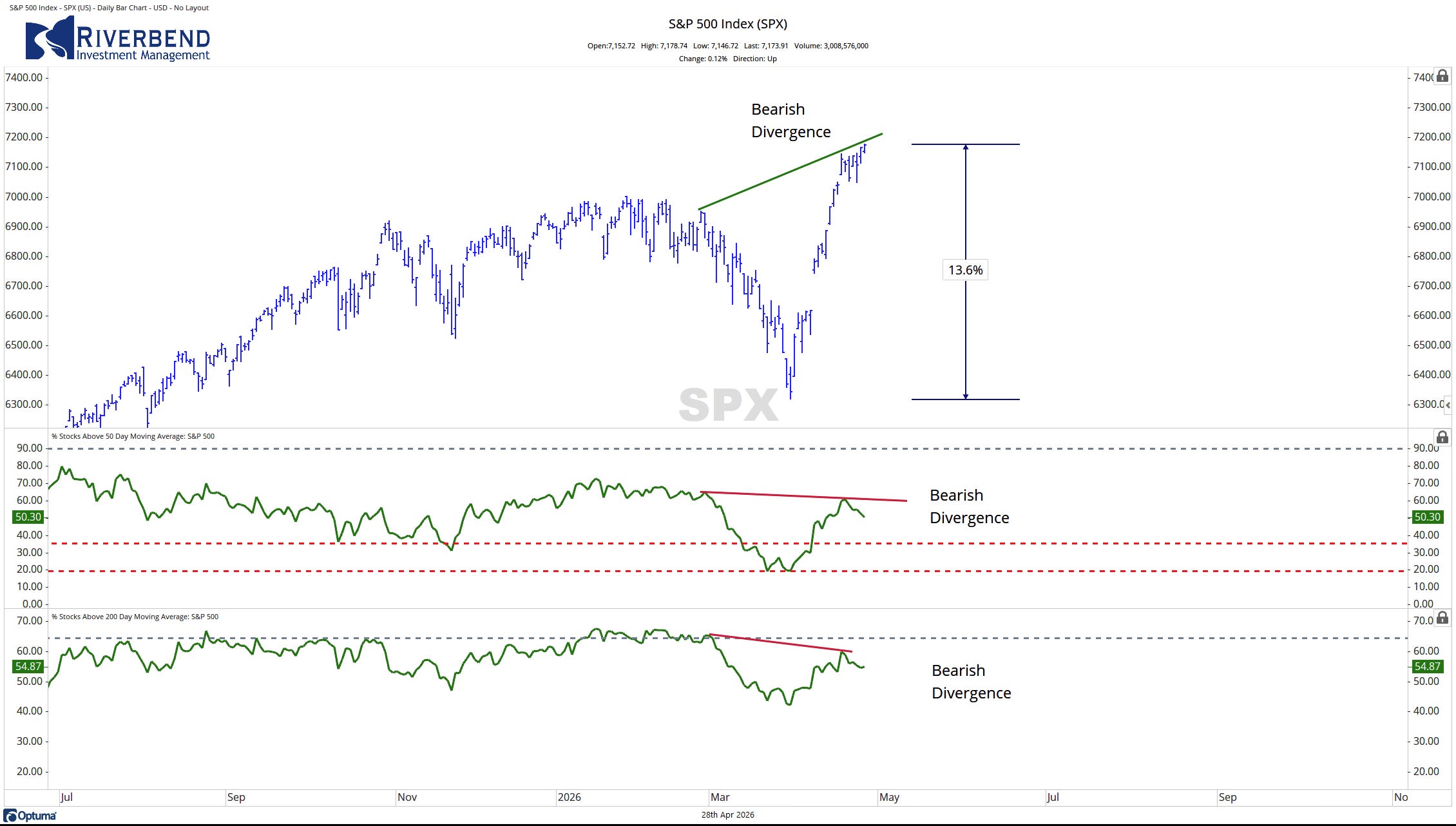

Since the March 30th low, the S&P 500 index has rallied over 13% to reach a new all-time high. However, it may be time for the market to take a bit of a pause to catch its breath.

Equities are looking a bit extended and are showing signs of exhaustion, at least in the short term.

For example, a bearish divergence is forming in the S&P 500 as the number of stocks above their respective 50 and 200-day moving average is declining while the index continues to rise.

In other words, fewer and fewer stocks are rising as the market rises.

Momentum Is Weakening

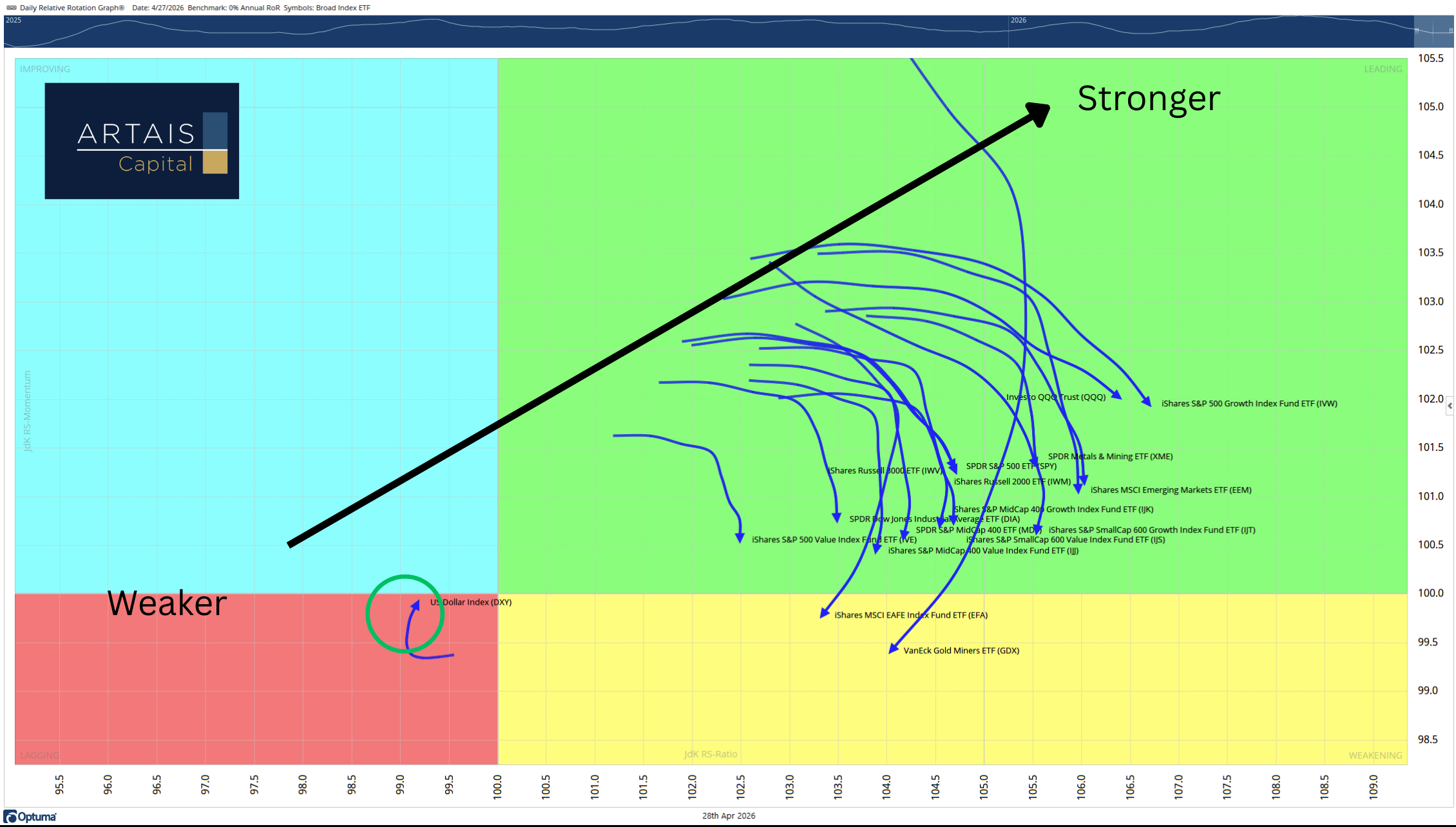

The RRG (relative rotation graph) for the broader market is also displaying signs of weakness.

Large, Mid, and Small Cap stocks are all rotating towards the “weakening” quadrant, indicating a loss of upside momentum.

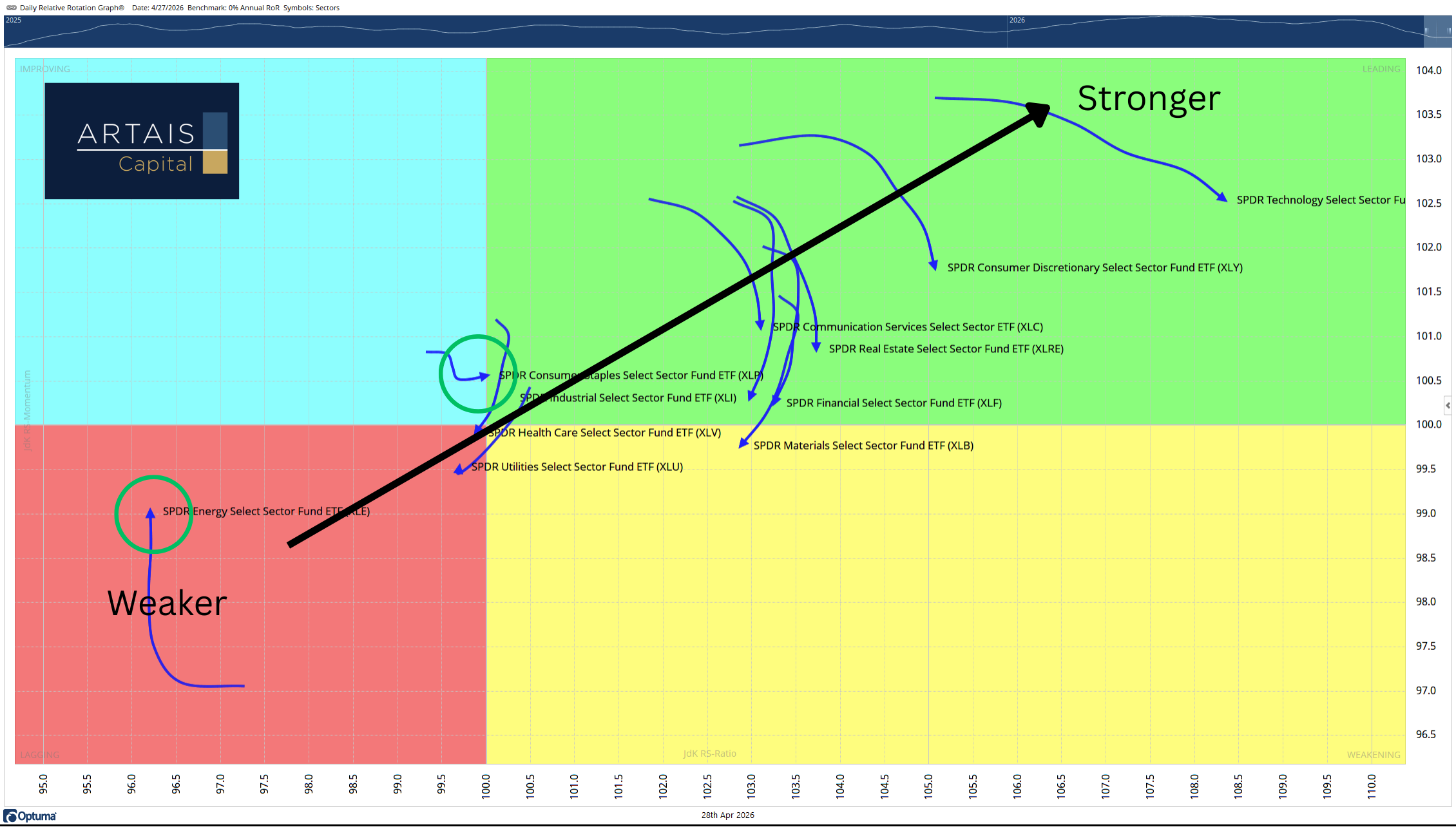

9 of the 11 sectors that make up the S&P 500 are also showing signs of weakness, with only the Energy and Consumer Staples sectors showing improvement:

So is it time to sell everything and head for the hills?

Not necessarily. I think a retest of the previous highs (the 7000 level for the S&P 500), followed by a stagnant summer market, is the more likely scenario.

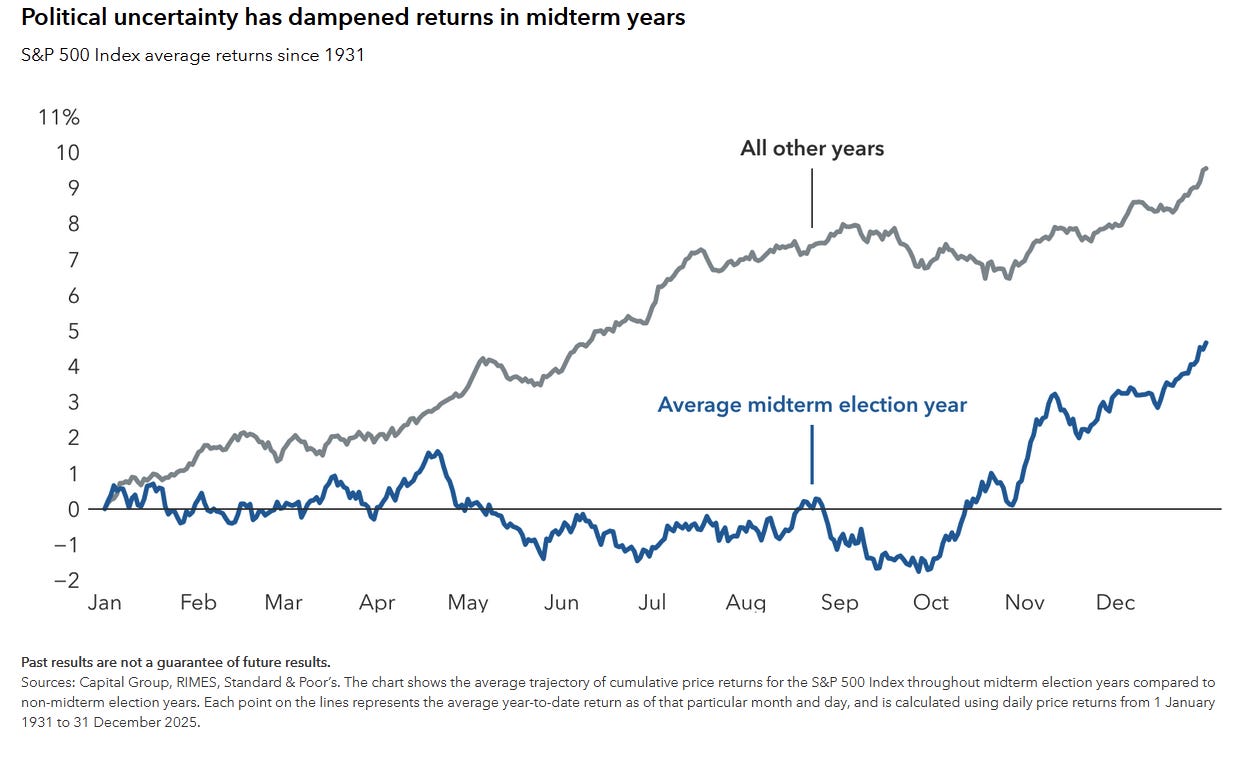

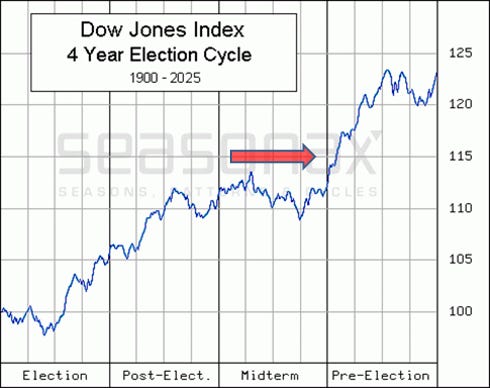

Don’t Forget About The 4-Year Election Cycle

During midterm election years in the US, stocks tend to consolidate as the November election approaches. Considering the current state of politics in the US, I wouldn’t be surprised if investors take a wait-and-see approach to their portfolios.

For those unfamiliar with the Presidential Cycle, the theory is based on the stock market's historical performance over a 4-year election cycle. Historically, midterm election years (2026) tend to perform the worst, while the pre-election year (2027) tends to perform the best:

The good news for investors: markets have historically rallied in the fourth quarter of midterm years, and the year that follows tends to be even stronger:

In short, this is a moment for patience, not panic. The combination of weakening internals, sector rotation toward defensives, and the historical headwinds of a midterm election year suggests the market may need time to consolidate before its next leg higher.

For now, staying selective and letting the data drive the decisions remains the most sensible way to navigate the months ahead.