Is It Time for Last Year's Winners to Make a Comeback?

Market rotation is starting to favor the old guard

Last fall, there was a shift in the market.

Stocks that had been leading the markets higher came to a screeching halt.

Names like Nvidia, Apple, and Google just stopped going up as fears of overvaluation and the impact that AI may have on other sectors of the market changed the narrative from “we are going to get massive growth from AI” to “AI is going to destroy a lot of companies.”

Areas like the software sector got crushed as investors began to worry that AI would be able to easily replicate and replace legacy software.

Names like Salesforce, Adobe, and ServiceNow became collateral damage in the AI disruption narrative.

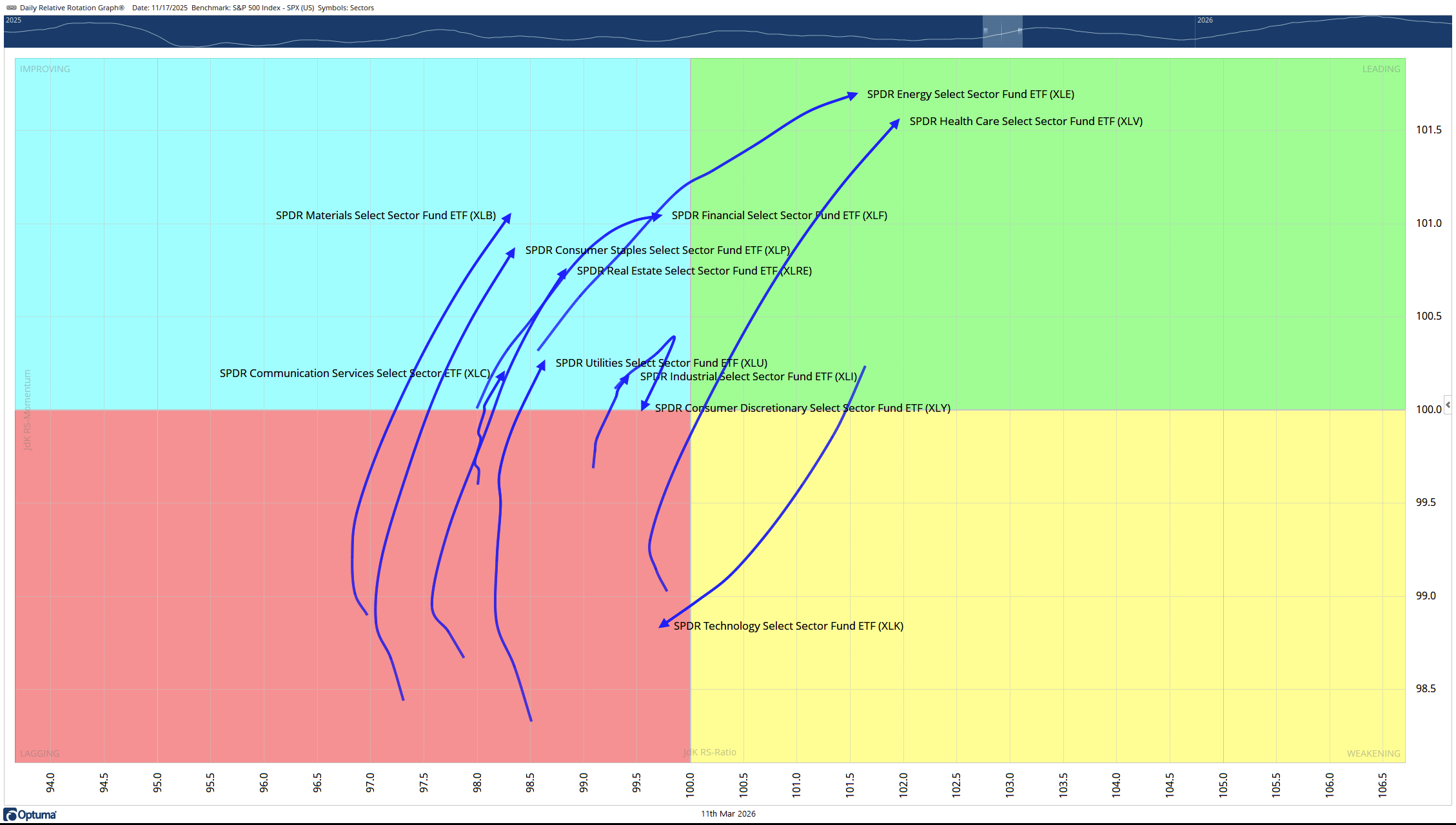

Value Takes the Lead: Industrials and Materials Surge

Value companies became the new leaders.

The Industrial and Materials sectors took off and saw an impressive rise during this time.

The rotation was textbook. As the RRG chart below shows, the technology sector was rotating into weakness while value and cyclical plays were accelerating toward strength.

Money was leaving one side of the market and flowing into the other.

Note: RRG Chart as of 11/17/2025

There were real catalysts behind this move. The passage of the “One Big Beautiful Bill Act” in early 2026 injected an estimated $137 billion in corporate tax reductions, with the largest benefits flowing to manufacturing and R&D.1

Companies like Caterpillar got re-rated as an “AI-adjacent” infrastructure play because its power generators became essential for the global buildout of AI data centers.

This was not just sentiment — it was fiscal policy lifting the real economy in a way that growth stocks could not capture.

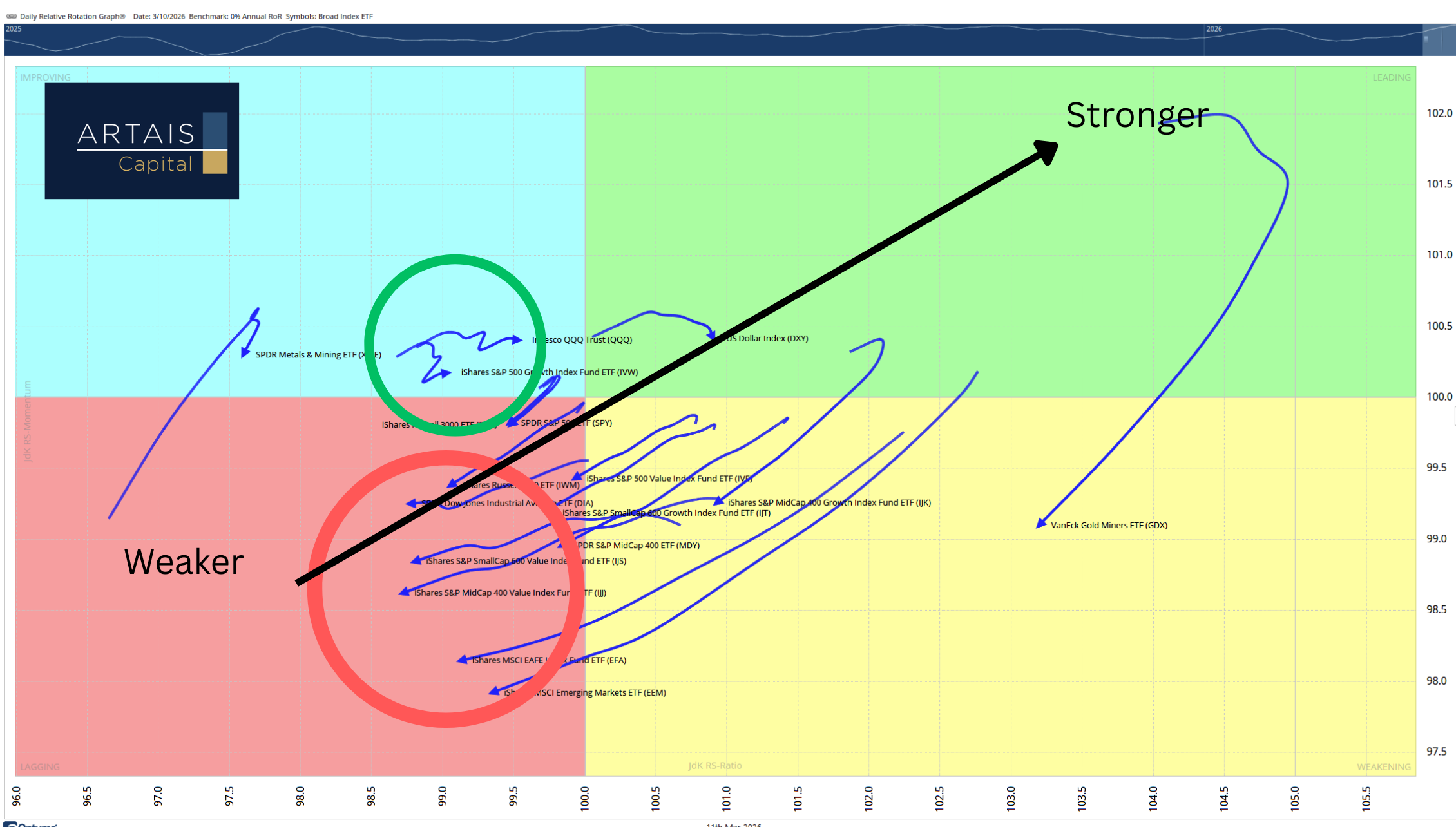

The Iran Catalyst: Why War Is Accelerating the Rotation Back to Tech

On February 28, 2026, U.S. and Israeli military forces launched strikes against Iran, setting off what has become the most significant geopolitical event since the Russian invasion of Ukraine.

The conflict has since expanded across the Middle East, pulling in Israel and disrupting global oil trade routes through the Strait of Hormuz.

The global markets immediately reacted.

Japan’s Nikkei 225 plunged more than 5%. South Korea’s KOSPI suffered its worst single-day decline on record, dropping over 12%. Oil prices spiked to nearly $120 a barrel. The average price of unleaded gasoline hit $3.54 per gallon — a 21% increase from a month earlier and the highest level since mid-2024.

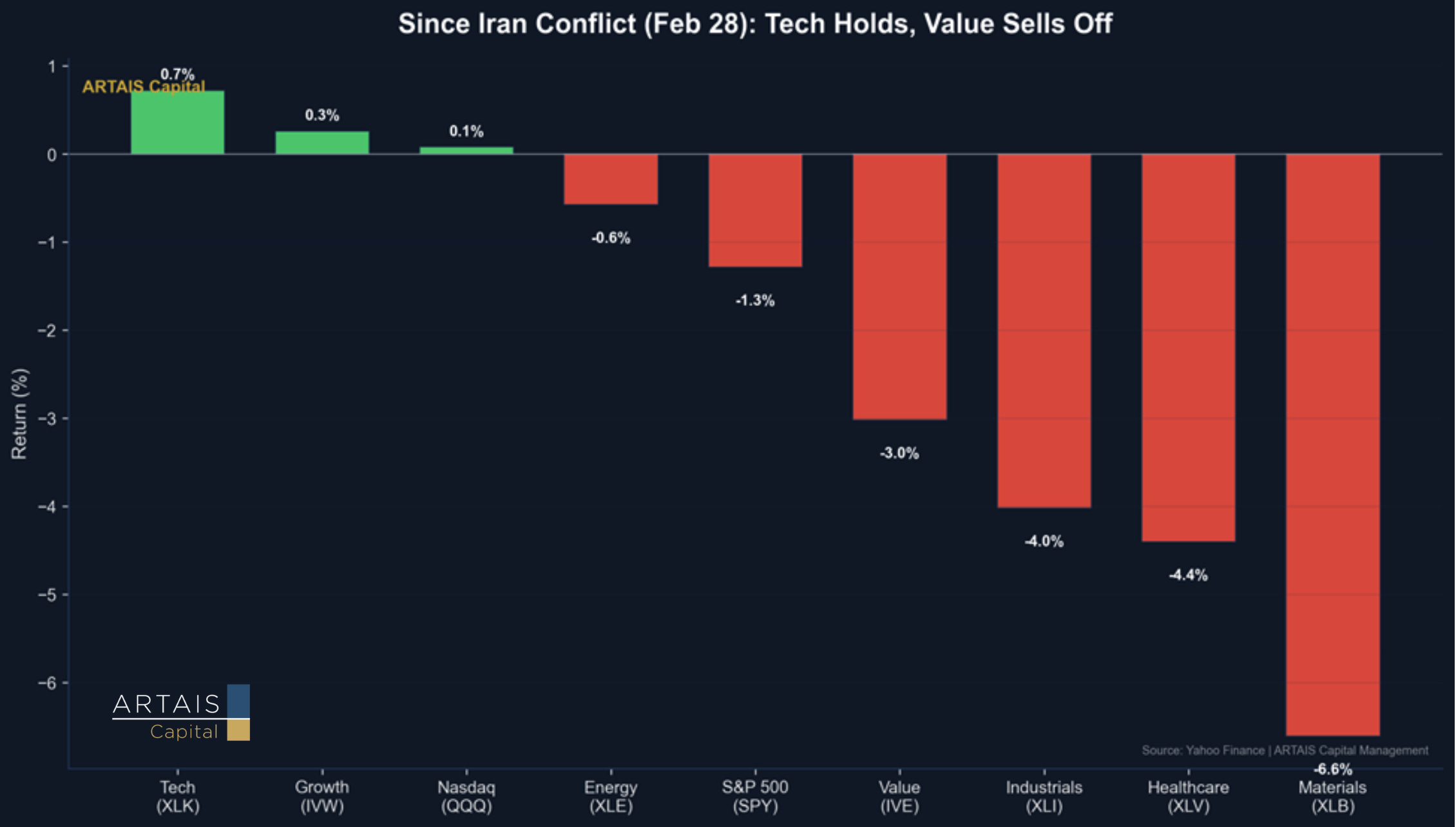

But here is what matters for portfolio positioning: the damage was not distributed equally across the market.

Tech and growth held up. Value and cyclicals did not.

Sector performance since the Iran conflict began (Feb 28, 2026). Source: Yahoo Finance / ARTAIS Capital Management

Why? Three reasons.

First, tech companies have minimal direct exposure to the conflict.

Unlike industrials and materials companies, which face rising input costs from spiking oil prices and supply chain disruptions through the Middle East, a software company’s cost structure is largely unaffected by crude prices.

Microsoft’s Azure margins do not change because oil hit $120. Google’s ad revenue does not decline because shipping lanes through the Strait of Hormuz are closed.

Second, after months of underperforming, tech valuations had corrected enough to look attractive again.

Morningstar noted that tech valuations were “sufficiently attractive to warrant investment,”2 and fund flow data showed sustained inflows into global tech funds even as the broader market sold off.

Third, flight to quality. When geopolitical uncertainty spikes, institutional capital gravitates toward large-cap, high-quality balance sheets.

Mega-cap tech — Apple, Microsoft, Google, Nvidia — fits that description better than any other corner of the market. These are companies with hundreds of billions in cash, minimal debt, and business models that generate free cash flow regardless of what happens in the Persian Gulf.

What Comes Next?

The key question is not whether tech can sustain a rally — the fundamentals and the flows both support it. The question is whether the conflict broadens in a way that overwhelms the flight-to-quality trade entirely and forces a broad de-risking across all sectors.

That scenario remains possible, but it is not what the data is showing today.

Until it does, the evidence points toward a continuation of this rotation back into growth and technology, with mega-cap quality names leading the way.

Staying tactical, watching the RRG signals, and resisting the urge to chase the value trade that the market may already be unwinding is the discipline this environment demands.

Happy trading,

John Rothe, CMT

ARTAIS Capital Management

john.rothe@artaiscapital.com

Disclaimer

ARTAIS Capital Management, LLC (“ARTAIS Capital”) is a registered investment advisor offering advisory services in registered states and in other jurisdictions where exempt. Registration does not imply a certain level of skill or training.

The information on this site is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This information should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal any performance noted on this site.

The information on this site is provided “AS IS” and without warranties of any kind, either express or implied. To the fullest extent permissible pursuant to applicable laws, ARTAIS Capital Management, LLC disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

Tax Foundation

Morningstar: https://global.morningstar.com/en-eu/markets/where-invest-iran-war-hits-global-stock-markets