When Missiles Fly, What Happens to Markets?

A Data-Driven Look at Stocks, Bonds, and Sectors After U.S. Military Strikes

“The stock market has predicted nine of the last five recessions.” — Paul Samuelson. But here’s what Samuelson didn’t say: it’s also priced in roughly zero of the last eight U.S. military strikes within six months.

This past weekend, the United States and Israel launched joint military strikes against Iran, killing Supreme Leader Ayatollah Ali Khamenei and multiple senior officials. It was the most significant direct U.S. military action against a sovereign nation since the Iraq War in 2003.

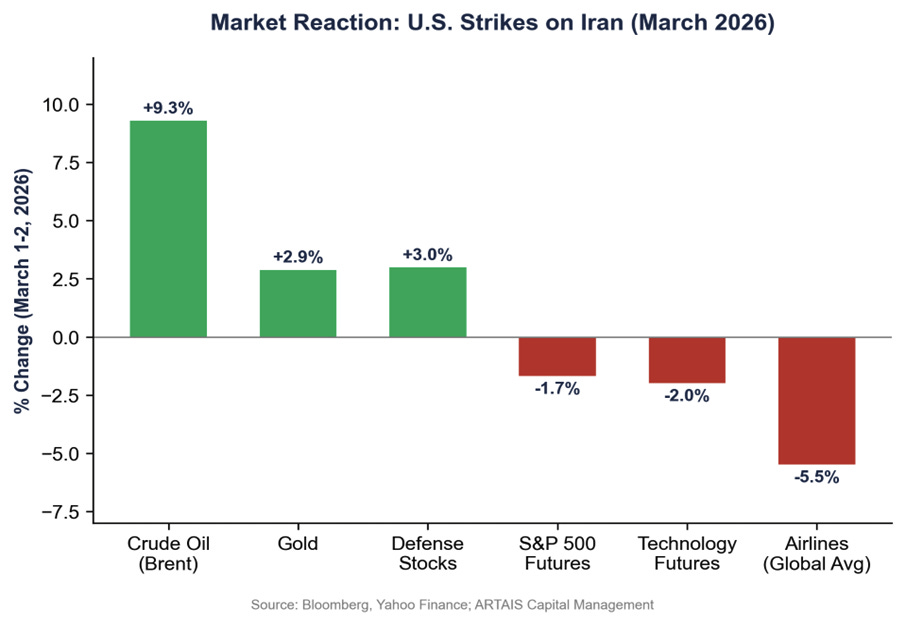

Markets reacted on cue: S&P 500 futures fell more than 1%. Brent crude surged over 9% toward $79 per barrel. Gold jumped nearly 3%. CNBC ran the banner: “MARKETS IN TURMOIL.”

If your instinct is to sell first and ask questions later, I understand it. But before you let headlines dictate your portfolio, let’s look at what actually happens to the stockmarket and specific sectors in the days, weeks, and months after the U.S. goes to war.

The data may surprise you.

What History Actually Shows: The Counterintuitive Evidence

Since World War II, the United States has launched military strikes, interventions, or full-scale operations more than a dozen times. The pattern in markets is remarkably consistent — and remarkably counterintuitive.

The First Week: Knee-Jerk Selling, Fast Recovery

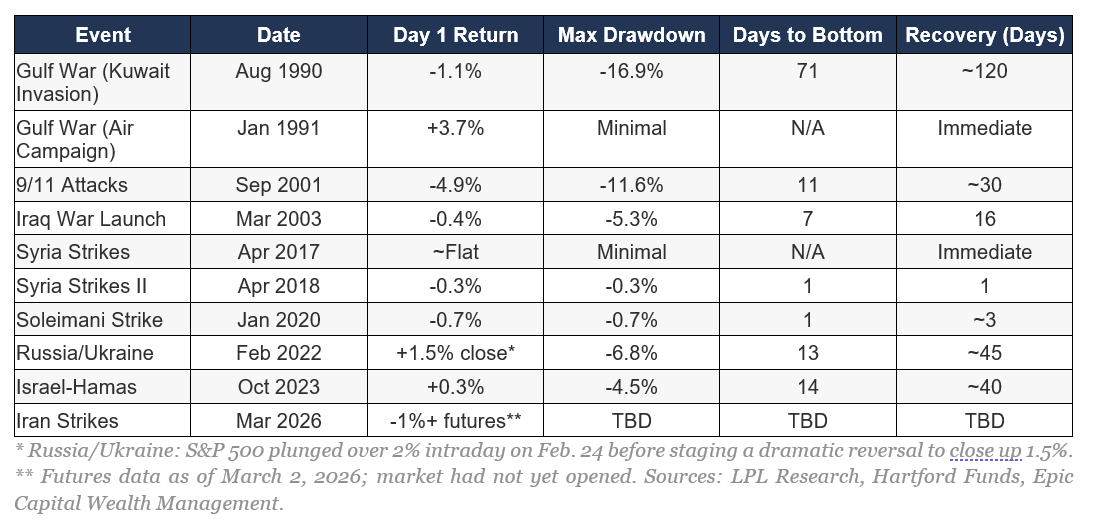

The average first-day S&P 500 decline following a major geopolitical military event is -1.1%. That’s it. One bad day. The average total drawdown from peak to trough is -4.7%, and it takes an average of just 19 trading days to find the bottom.

The average recovery from the bottom back to prior highs? 42 trading days — roughly two months.

Here’s what specific conflicts looked like:

Note: Historical returns are provided for educational context only. Past performance is not indicative of future results. Every conflict is unique, and there is no guarantee that future market reactions will mirror historical patterns. All investments involve risk, including the possible loss of principal.

Notice the pattern: The biggest drawdowns occurred when military events coincided with existing economic weakness (the 1990 Kuwait invasion happened during a recession; 9/11 happened during the dot-com bust). When the economy was healthy, markets shrugged off the missiles within days.

One Month Out: Essentially Flat

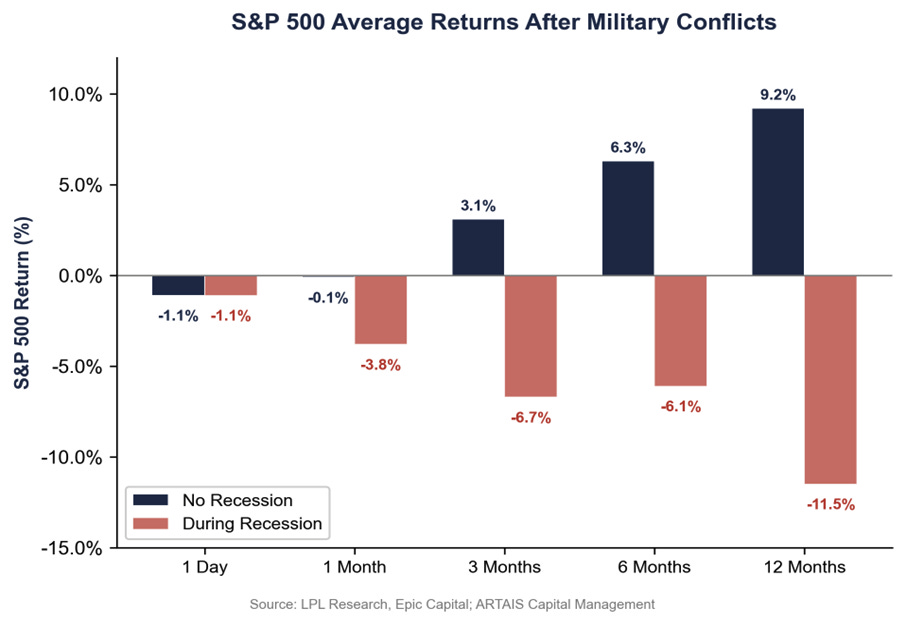

At the one-month mark after military events, the S&P 500 has averaged a return of approximately -0.1% when no recession is present. During the 2003 Iraq War, the DJIA rose 8.4% in the month following the invasion. After the 2020 Soleimani strike, markets recovered their losses within approximately 72 hours.

The critical variable is not the conflict itself — it’s whether the conflict triggers or coincides with an economic recession. When it doesn’t, markets barely notice.

Six Months Out: The Real Story Emerges

At six months, the picture has historically turned decisively positive. The S&P 500 has averaged approximately +6.3% in the six months following military conflicts when the economy avoids recession. During recessionary periods, the six-month return averaged -6.1%.

After the 1991 Gulf War air campaign, the S&P 500 was up roughly 15% six months later. After the 2003 Iraq invasion, stocks were well on their way to a 26.7% annual gain. After the 2017 Syria strikes, the S&P 500 barely paused before continuing its bull market run.

Note: Historical returns are provided for educational context only. Past performance is not indicative of future results. Every conflict is unique, and there is no guarantee that future market reactions will mirror historical patterns. All investments involve risk, including the possible loss of principal.

The historical takeaway: when the underlying economy has been sound, military conflicts have created buying opportunities, not lasting damage. That said, every conflict is unique, and past patterns provide context — not guarantees.

The Drawdown Playbook: How Deep Have Markets Fallen?

The depth of the initial selloff depends heavily on the scale and perceived risk of the conflict. Limited strikes have produced minimal drawdowns. Major invasions or conflicts that threaten global economic infrastructure have caused deeper pullbacks.

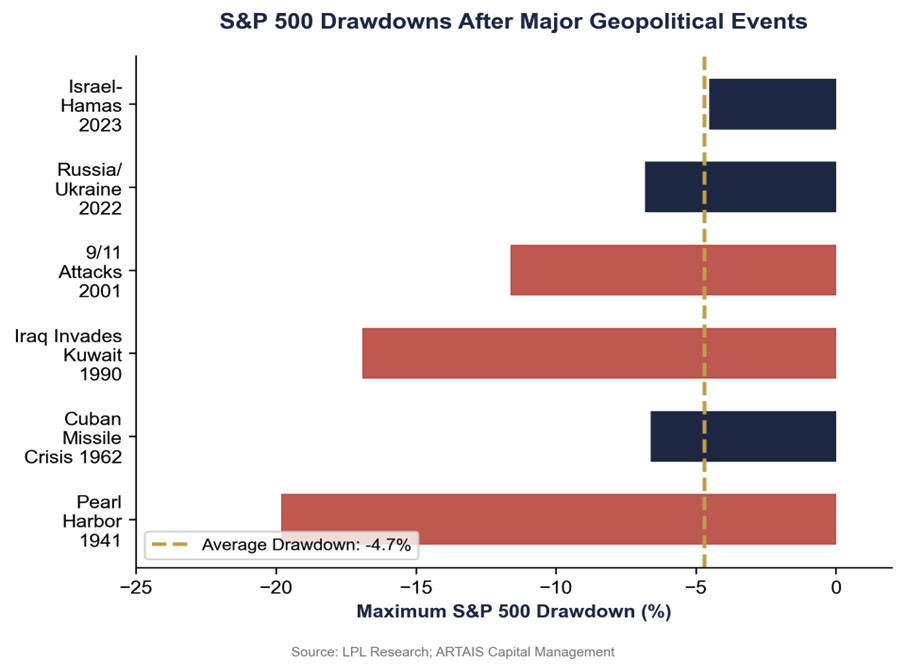

The average drawdown across major geopolitical events since World War II is approximately -4.7%. Pearl Harbor and the Iraqi invasion of Kuwait stand out as outliers because they represented existential threats to U.S. security or global oil supply. Limited strikes like Syria in 2017 or the Soleimani operation barely registered.

The current Iran situation falls somewhere in between: it’s more significant than a limited strike (the killing of a head of state is unprecedented in modern U.S. military action), but the economic risk depends entirely on what happens to the Strait of Hormuz.

Winners and Losers: The Sector Rotation Playbook

Military conflicts have historically triggered predictable rotations across sectors. Some tend to win immediately.

Others tend to suffer.

The magnitude depends on the conflict’s impact on energy markets and economic growth expectations.

Historical Winners

Energy (+8-10% in the first 48 hours)

Energy is the most direct beneficiary of Middle East conflicts. Brent crude surged over 9% toward $79; WTI climbed over 9% to roughly $73. If the Strait of Hormuz sees sustained disruption, J.P. Morgan estimates oil could test $100 or higher. Energy equities (XLE) have historically outperformed during Middle East conflicts because the same supply fears that pressure the broader economy tend to directly boost energy sector revenues.

Defense & Aerospace (+2-3% initial, with potential longer tailwind)

Lockheed Martin, Northrop Grumman, and RTX have been standout performers in 2025-2026. The iShares U.S. Aerospace & Defense ETF (ITA) is up approximately 14% year-to-date, with a roughly 35% surge since the first strikes on Iranian nuclear facilities last June. Defense stocks often spike at the onset of a conflict — and unlike some geopolitical trades, this sector can benefit from a longer-term tailwind because military spending commitments tend to extend for years.

Gold & Precious Metals (+2-3%)

Gold jumped approximately 2.9% to roughly $5,391 per ounce. When bonds can’t serve as the safe haven (as in this current inflationary scenario), gold has historically filled the void. Gold miners (GDX) tend to amplify gold’s moves with additional leverage.

Utilities & Consumer Staples (Relative Defensive Stability)

Traditional defensive sectors don’t typically surge, but they have historically provided relative stability. Utilities and consumer staples tend to outperform on a relative basis during periods of elevated geopolitical uncertainty because their earnings are generally less sensitive to economic cycles and energy costs.

Historical Losers

Airlines & Travel (-5-7% or more)

Airlines have historically been the most immediate casualty of military conflicts. In the current situation, over 50% of global flights to the Middle East were cancelled within hours of the strikes. Qantas plunged as much as 10% before recovering to close down approximately 6%. ANA and Japan Airlines dropped more than 5%. IAG (British Airways parent) fell nearly 7%. Airlines face a triple threat: surging jet fuel costs, route disruptions, and reduced consumer travel demand.

Technology (-2% or more)

Tech stocks led the futures selloff with Nasdaq futures down approximately 2%. High-growth technology companies tend to be rate-sensitive, and if oil-driven inflation pushes yields higher (which is already happening), their valuations may compress. Additionally, any conflict that threatens global supply chains raises concerns for semiconductor and hardware companies with Asian manufacturing exposure.

Consumer Discretionary

Higher energy prices function as a tax on consumers. When gasoline prices rise, spending on discretionary items tends to fall. Restaurants, retailers, and auto manufacturers have historically underperformed when oil spikes.

Financials (Mixed, Trending Negative Short-Term)

Banks face a complicated picture. Higher interest rates could boost net interest margins, but increased credit risk, potential loan defaults in energy-sensitive regions, and general risk-off sentiment have historically pushed financials lower in the first weeks of a conflict.

The Critical Variable: Does This Cause a Recession?

Here’s the single most important question for your portfolio right now — and it’s not “will we go to war?” We’re already there.

The question is: Does this conflict tip the U.S. economy into recession?

The historical data has been unambiguous on this point:

Note: Historical returns are provided for educational context only. Past performance is not indicative of future results. Every conflict is unique, and there is no guarantee that future market reactions will mirror historical patterns. All investments involve risk, including the possible loss of principal.

The spread between these two historical outcomes is enormous: +9.2% versus -11.5% at the 12-month mark. That’s a 20-percentage-point gap driven entirely by whether the economy held up.

The Recession Risk Factors to Watch

Oil above $100/barrel: Historically, this represents a potential stagflation threshold. Every $10 increase in oil has tended to shave roughly 0.1-0.2% off GDP growth and add 0.2-0.3% to inflation.

Strait of Hormuz closure: Would represent a genuine economic shock. 20% of the global oil supply transits this chokepoint daily. A sustained closure could push oil to $120-130, according to J.P. Morgan estimates.

Conflict duration: Limited strikes (days to weeks) have historically had minimal economic impact. Prolonged military campaigns (months) have tended to affect consumer confidence and business investment.

Federal Reserve response: If oil-driven inflation forces the Fed to maintain or raise rates during a growth slowdown, the recession probability could increase significantly.

The Skeptic’s Corner: Why This Time Could Be Different

Before concluding that history guarantees a market recovery, consider the counterarguments:

1. Iran is not Iraq, Syria, or Libya.

Iran is the world’s sixth-largest oil producer and controls access to the Strait of Hormuz. Previous U.S. military actions targeted countries with limited ability to disrupt global energy markets. Iran has that ability.

2. The killing of a head of state is unprecedented.

The Soleimani strike killed a military commander. These strikes killed the Supreme Leader. The geopolitical escalation risk is categorically different, and the path to de-escalation is far less clear.

3. Markets were already fragile.

The S&P 500 closed at approximately 5,955 on February 27, already dealing with hot inflation data and fading AI optimism. This is not a market striking from all-time highs with maximum confidence.

The ARTAIS Perspective: What We’re Watching

At ARTAIS Capital, we don’t predict whether conflicts will escalate or resolve. We aim to respond to what the data and our indicators tell us in real time.

Here’s my framework for navigating this environment:

1. Monitor the Technical Signals

Our rules-based approach using the Ichimoku Cloud, PMO, and momentum indicators is designed to tell us whether the broader trend remains intact or is breaking down. If the S&P 500 breaks below key cloud support levels, our process may reduce equity exposure — not because of headlines, but because the price action warrants it.

2. Watch Oil, Not Just Stocks

The Strait of Hormuz is the real risk variable. If tanker traffic resumes and oil pulls back below $75, the conflict’s economic impact may be contained. If oil sustains above $85-90, the recession probability rises materially.

3. Sector Positioning Matters

The divergence between winning and losing sectors is unusually wide. Energy, defense, and gold may offer tactical opportunities. Airlines, tech, and consumer discretionary face headwinds. A tactical approach that can shift sector exposure may have a meaningful advantage over a static allocation in this environment.

4. Don’t Sell Into Panic

The historical evidence has been overwhelming: selling on the first day of a military conflict has been the wrong trade in nearly every instance over the past 80 years. The average historical recovery time is 42 trading days. Panic selling has historically locked in losses at exactly the wrong moment.

What Comes Next

This week, markets will attempt to price in the duration and scope of U.S. military operations in Iran. The Monday open will set the initial tone, but the real story will unfold over weeks and months.

I’ll be watching the technical levels, the oil markets, and the bond market’s unusual behavior for signals about what comes next. If history is any guide, the buying opportunity may be right in front of us — but only if the economy holds.

John Rothe, CMT

Founder, Portfolio Manager

ARTAIS Capital Management

3/2/26

Disclaimer

ARTAIS Capital Management, LLC (“ARTAIS Capital”) is a registered investment advisor offering advisory services in registered states and in other jurisdictions where exempt. Registration does not imply a certain level of skill or training.

The information on this site is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This information should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal any performance noted on this site.

The information on this site is provided “AS IS” and without warranties of any kind, either express or implied. To the fullest extent permissible pursuant to applicable laws, ARTAIS Capital Management, LLC disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.