Your Portfolio Was Built for a World That Ended Last Week

Oil above $100. Negative Jobs. A Frozen Fed. Three Things That Weren't Supposed to Happen at the Same Time, Just Did. Here's My Bull/Bear Case and What I am Watching Right Now.

What’s Actually Happening

Let’s dispense with the euphemisms. Markets aren’t “experiencing volatility” — they’re repricing for a world where 20% of global oil supply is offline, and the US economy is shedding jobs.

Those are two things that aren’t supposed to happen at the same time.

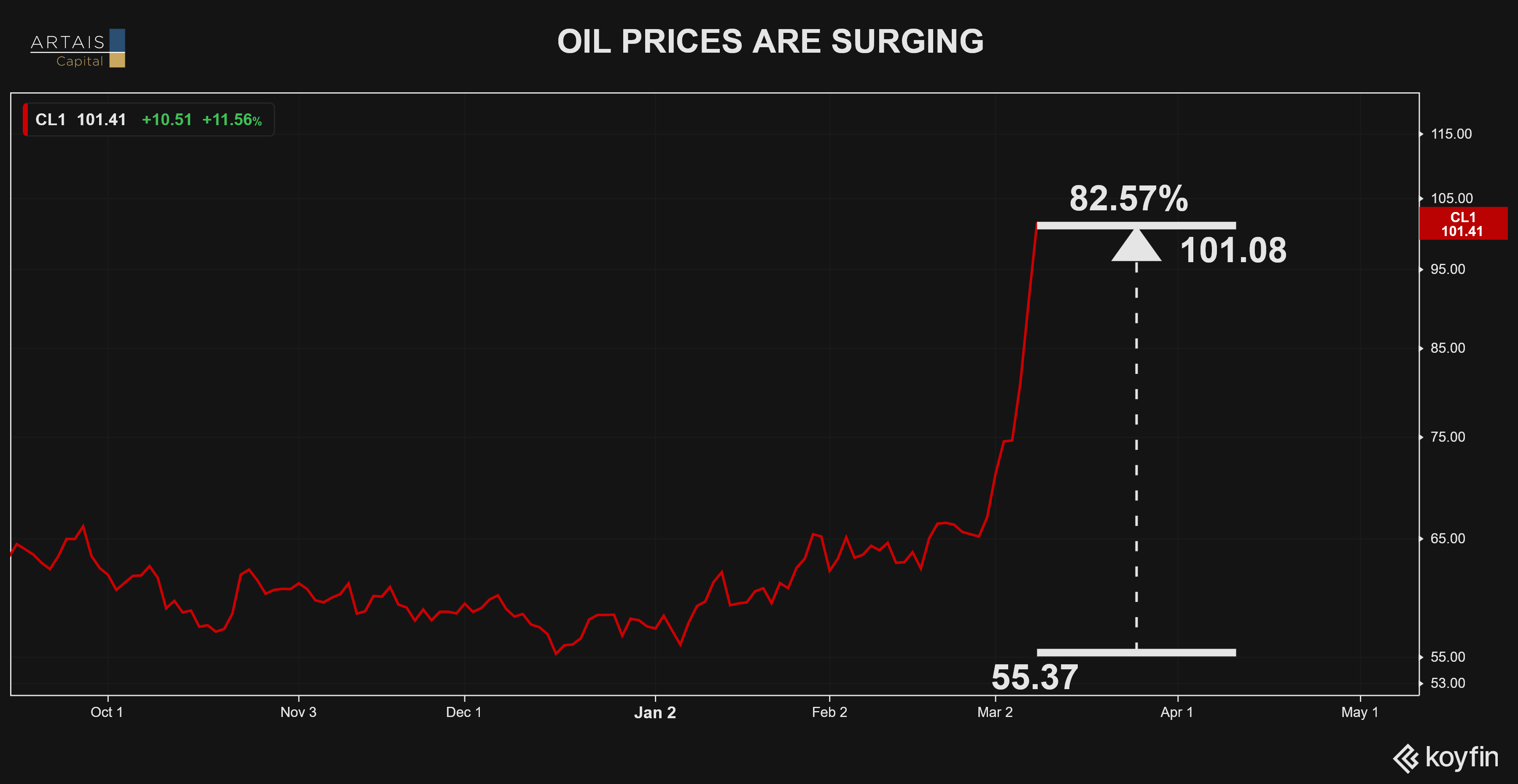

The Iran war, now entering its second week, has effectively closed the Strait of Hormuz — the narrow waterway through which a quarter of the world’s seaborne oil passes.

WTI crude has surged to $107 a barrel. Brent briefly topped $119. Qatar declared force majeure on its liquefied natural gas exports after Iranian strikes on the Ras Laffan complex. Saudi Arabia’s Ras Tanura refinery — the largest in the Middle East — shut down as a precaution after drone interception debris caused a fire. Gas at the pump is heading to $4 a gallon, and diesel has doubled in Europe.

This is not a speculative spike driven by fear — it’s a physical supply crisis with cascading second-order effects.

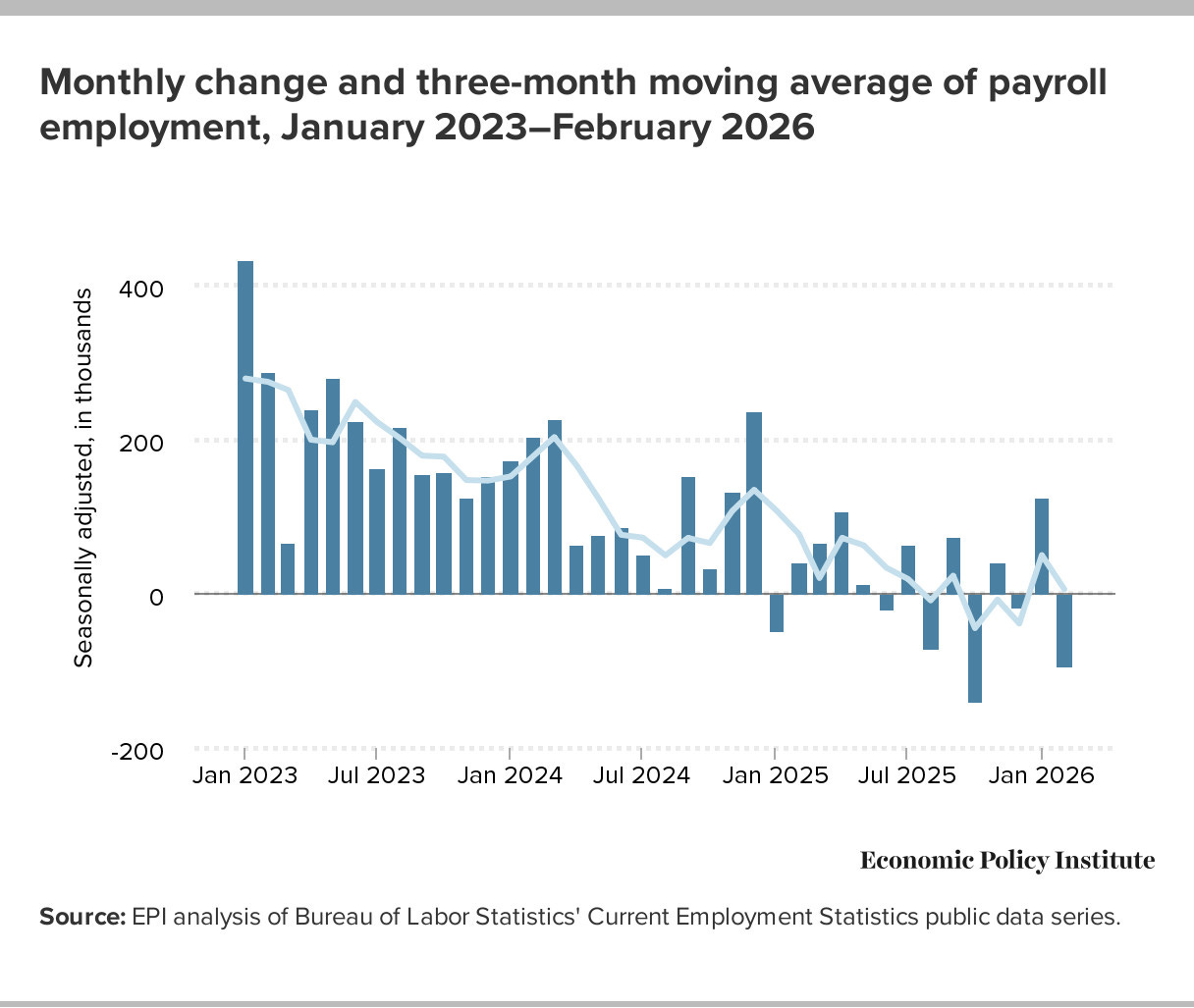

Then came Friday’s jobs report: the economy lost 92,000 jobs when economists expected it to add 55,000.

The word no one in Washington or on Wall Street wants to say out loud is now unavoidable: stagflation.

Healthcare — a historically resilient sector — shed 28,000 positions, though a Kaiser Permanente strike affecting over 30,000 workers in Hawaii and California accounted for much of that decline.

Strip out the strike, and the underlying picture is still soft — but the headline number overstates the structural weakness. The unemployment rate ticked up to 4.4%. The word no one in Washington or on Wall Street wants to say out loud is now unavoidable: stagflation.

The Pain Investors Are Feeling Right Now

What makes this moment particularly difficult is that there’s no obvious playbook.

In a normal correction, you can point to an overvalued market that needs to reset, or a Fed that’s been too tight, or earnings that missed expectations.

Those are problems with identifiable solutions. This is different.

This is a supply-side shock layered on top of a weakening labor market, and it’s happening while the Federal Reserve is paralyzed.

Cut rates, and you pour fuel on energy-driven inflation.

Hold rates, and you watch the job market deteriorate.

The Fed “put” — that implicit backstop that has bailed out investors in every downturn since 2009 — doesn’t work when the problem is bombs and barrels, not balance sheets.

For the investor who built a “diversified” portfolio of US equities, international stocks, and bonds, the math is unforgiving this month.

Equities are down across the board. International markets are getting hit harder by the energy shock. Bonds are rallying modestly, but not enough to offset equity losses.

The only things working are energy stocks, gold at $5,125 an ounce, and cash.

True diversification, it turns out, requires the ability to own none of the above when they’re all going the wrong direction.

And that’s the quiet pain that no allocation chart or Monte Carlo simulation prepares you for: the realization that “staying the course” is indistinguishable from “doing nothing” when the course itself has changed.

The Bull Case — Why This Could Resolve

Before we write the obituary for this bull market, the evidence for resolution deserves honest consideration.

First, geopolitical oil spikes have historically reversed within three to six months as demand destruction, strategic petroleum reserve releases, and diplomatic efforts combine to cap prices.

Second, the VIX is strikingly low for a crisis of this magnitude, suggesting either complacency or that the market sees a resolution ahead.

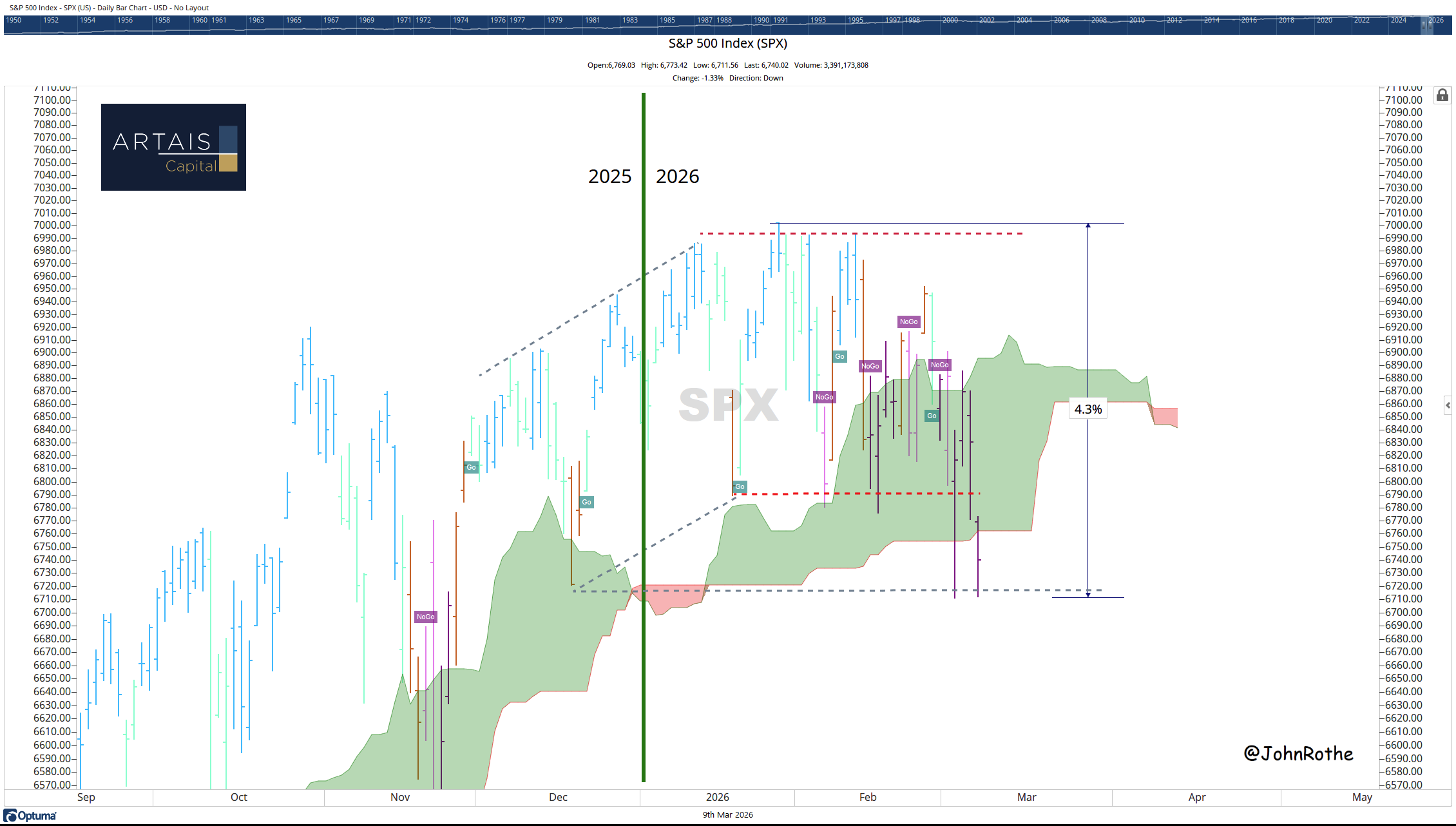

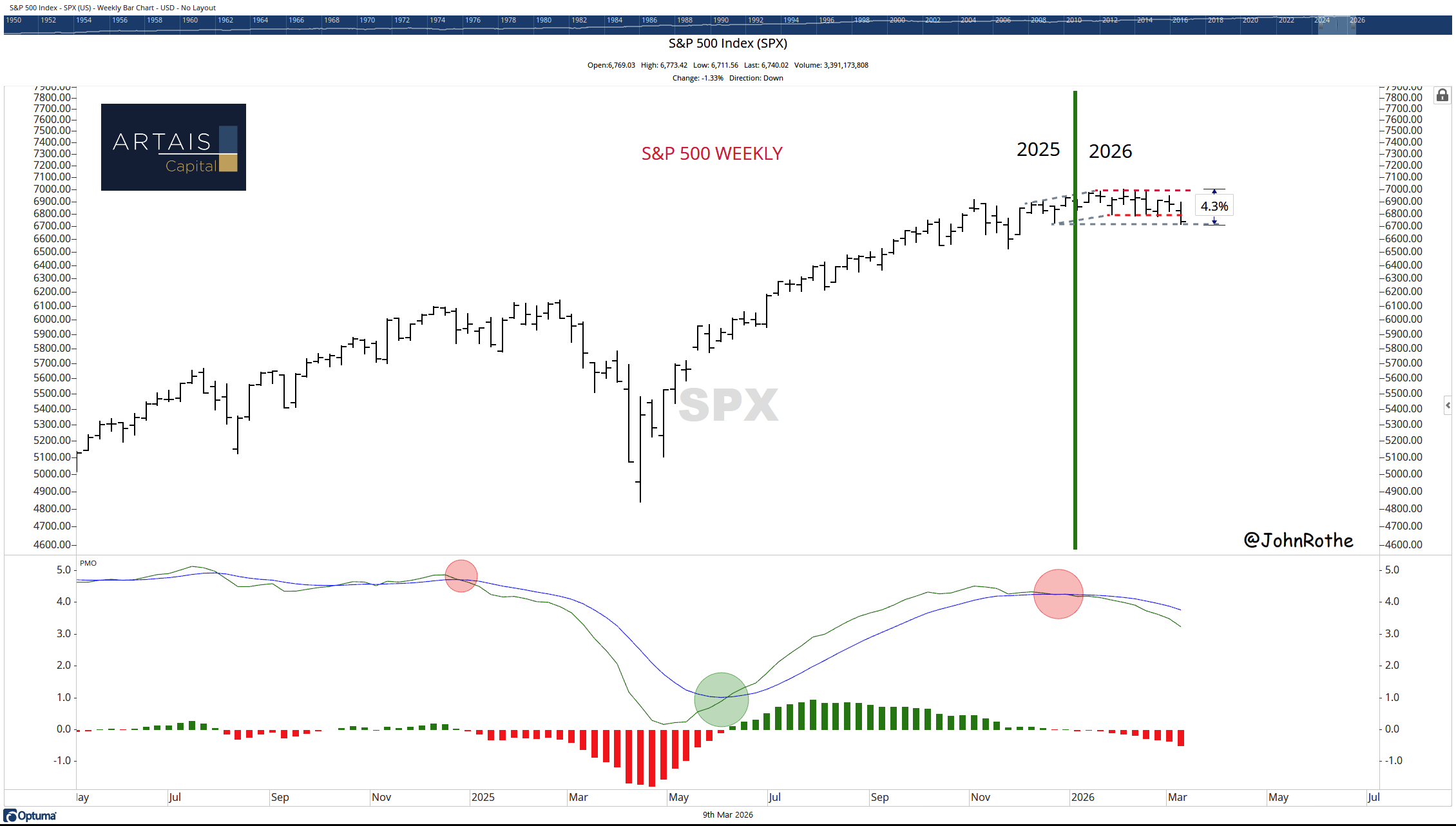

Third, the S&P 500 has not broken its 200-day moving average. Every correction in this cycle that held that level produced a meaningful bounce.

Fourth, the weak jobs data actually strengthens the case for Fed rate cuts — the March 17–18 FOMC meeting could deliver a dovish pivot that sparks relief.

And fifth, corporate earnings growth remains positive; this is an exogenous shock, not an earnings recession.

The bull case requires things to go right — de-escalation, Hormuz reopening, a cooperative Fed. That’s a lot of “ifs.”

The Bear Case — Why This Could Get Worse

The bear case requires only that the current trajectory continue.

Twenty percent of the global oil supply offline is unprecedented in modern markets.

Even if a ceasefire materializes tomorrow, the infrastructure damage to Saudi and Qatari facilities will take months to repair.

Meanwhile, the consumer spending cliff is approaching fast — $4 gas plus a deteriorating job market is a double squeeze on household budgets that shows up in earnings within one to two quarters.

The technical damage is real and accelerating.

The S&P 500 has broken below its 50-day moving average. The weekly Price Momentum Oscillator is turning down — historically a signal of sustained downtrends, not buyable dips.

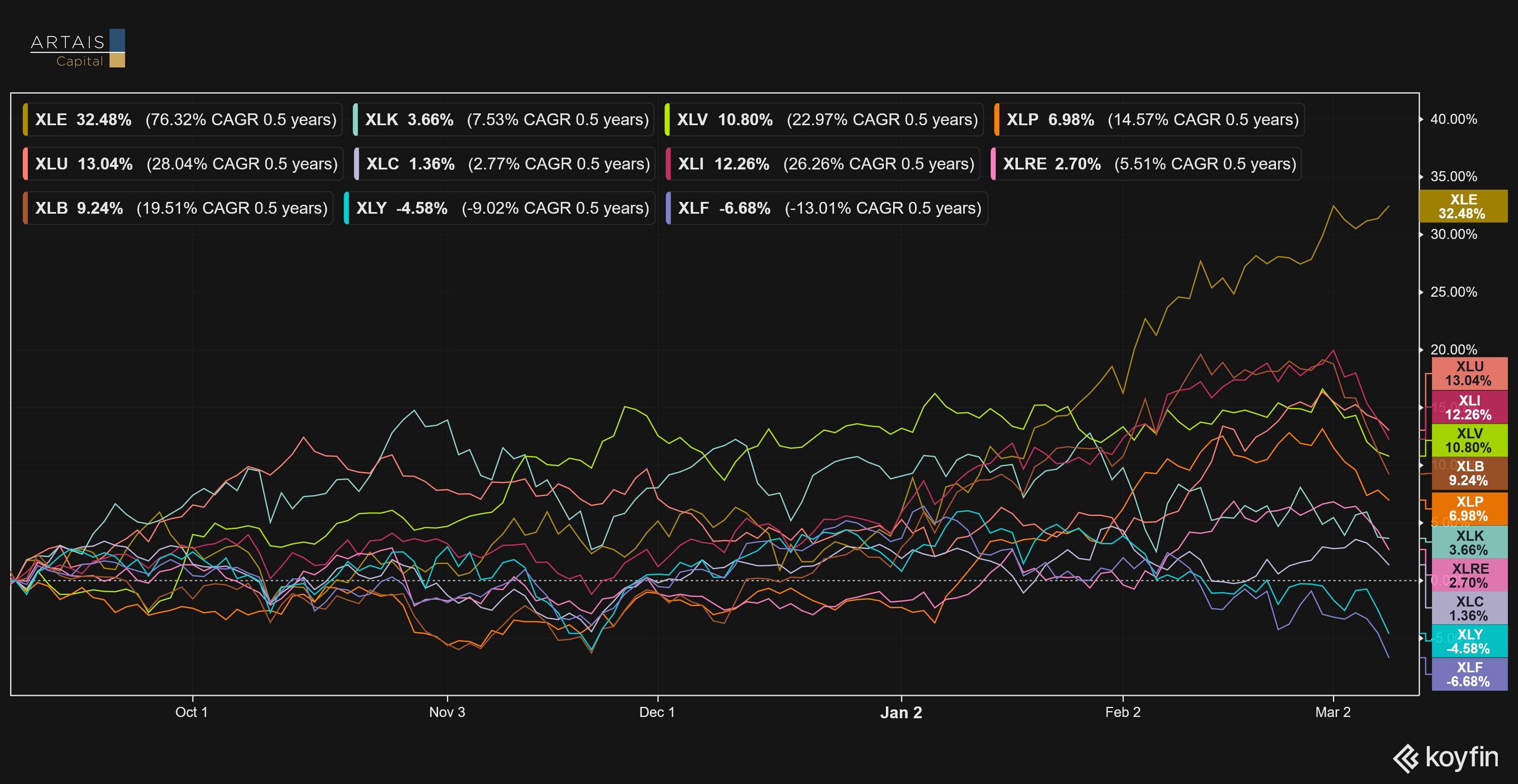

Sector breadth is narrowing to just energy, and narrow leadership in a declining market is one of the most reliable bearish signals in technical analysis.

What To Watch

Despite the recent volatility, tech stocks have been holding up better than the rest of the market.

Since last Fall, tech stocks have been underperforming most value sectors within the market. But the tech sector has been trading in a sideways range. Not getting weaker, not getting stronger.

Instead, the sector has been consolidating/absorbing the gains from 2025:

Last year’s big winner was NVIDIA. Currently, the stock is stuck in the same sideways trading pattern.

The extended sideways trading range can lead to a next leg up for AI stocks. I believe the opportunity is too great to ignore, and we may start seeing the shift back into these sectors as traders take profits from the energy sector.

Due to the large weighting of the technology sector within the S&P 500, this can potentially push the S&P 500 higher and out of its trading range.

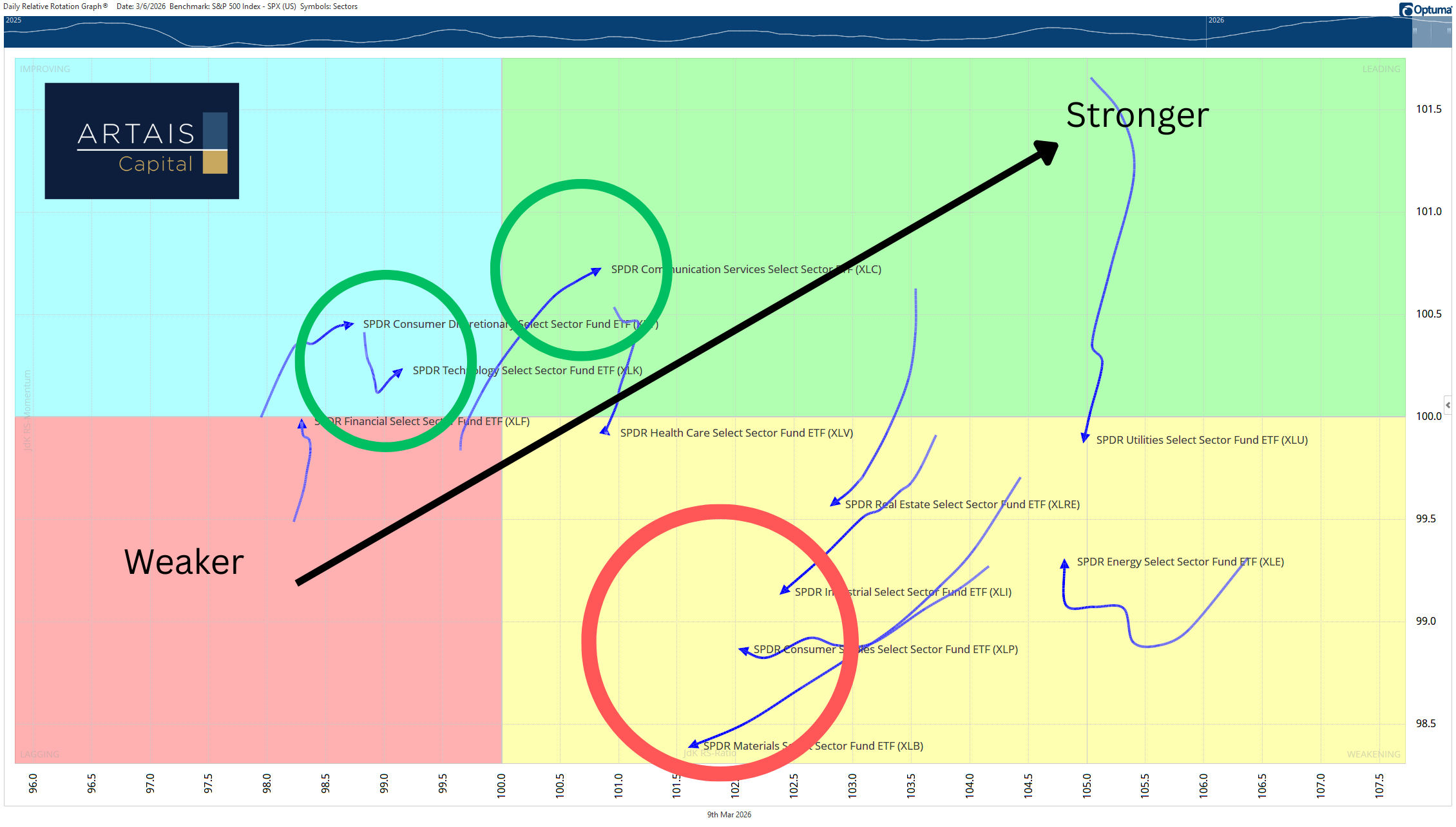

I am keeping a close eye on sector rotation. Already, the rotation within the market is starting.

The Relative Rotation Graph(RRG) for the sectors within the S&P 500 is already showing a rotation that is favoring tech and communication sectors, while value sectors like materials and industrial are rotating towards weakness:

Conclusion

It’s going to be up to last year’s winners to give direction to this market. If investors believe the overall bull market theme remains intact, then we should start seeing opportunistic investors looking for bargains.

If they don’t step in this week, then Wall Street will need to revisit and reprice their 5 year outlooks, which will cause major disruption to the US markets.

Happy trading,

John Rothe, CMT

ARTAIS Capital Management

john.rothe@artaiscapital.com

Disclaimer

ARTAIS Capital Management, LLC (“ARTAIS Capital”) is a registered investment advisor offering advisory services in registered states and in other jurisdictions where exempt. Registration does not imply a certain level of skill or training.

The information on this site is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This information should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal any performance noted on this site.

The information on this site is provided “AS IS” and without warranties of any kind, either express or implied. To the fullest extent permissible pursuant to applicable laws, ARTAIS Capital Management, LLC disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.