Cheaper Oil is Coming. What Does it Mean for Inflation and Your Portfolio?

Plus: which areas performed well after an oil spike - and why.

Four months ago, the most important number in the world was the width of a shipping lane. The Strait of Hormuz — twenty-one miles across at its narrowest — carries roughly a fifth of the oil the world uses every day.

When the conflict with Iran shut the Strait in late February, the price of crude did what it always does when there is a conflict in the Middle East: it went straight up.

This week, the channel is (hopefully) reopening.

A tentative framework to end the war and lift the U.S. naval blockade is headed for signing, oil has given back almost the entire war premium, and the relief is already working its way into prices at the pump.

That’s the headline, and the headline is good news. But it’s more complicated than just a headline.

The more useful question isn’t “Is oil going down?”

It’s “What does cheaper oil set in motion — who it helps, what it does to inflation and the Fed, and which part of the energy story doesn’t actually care about the price of a barrel at all.”

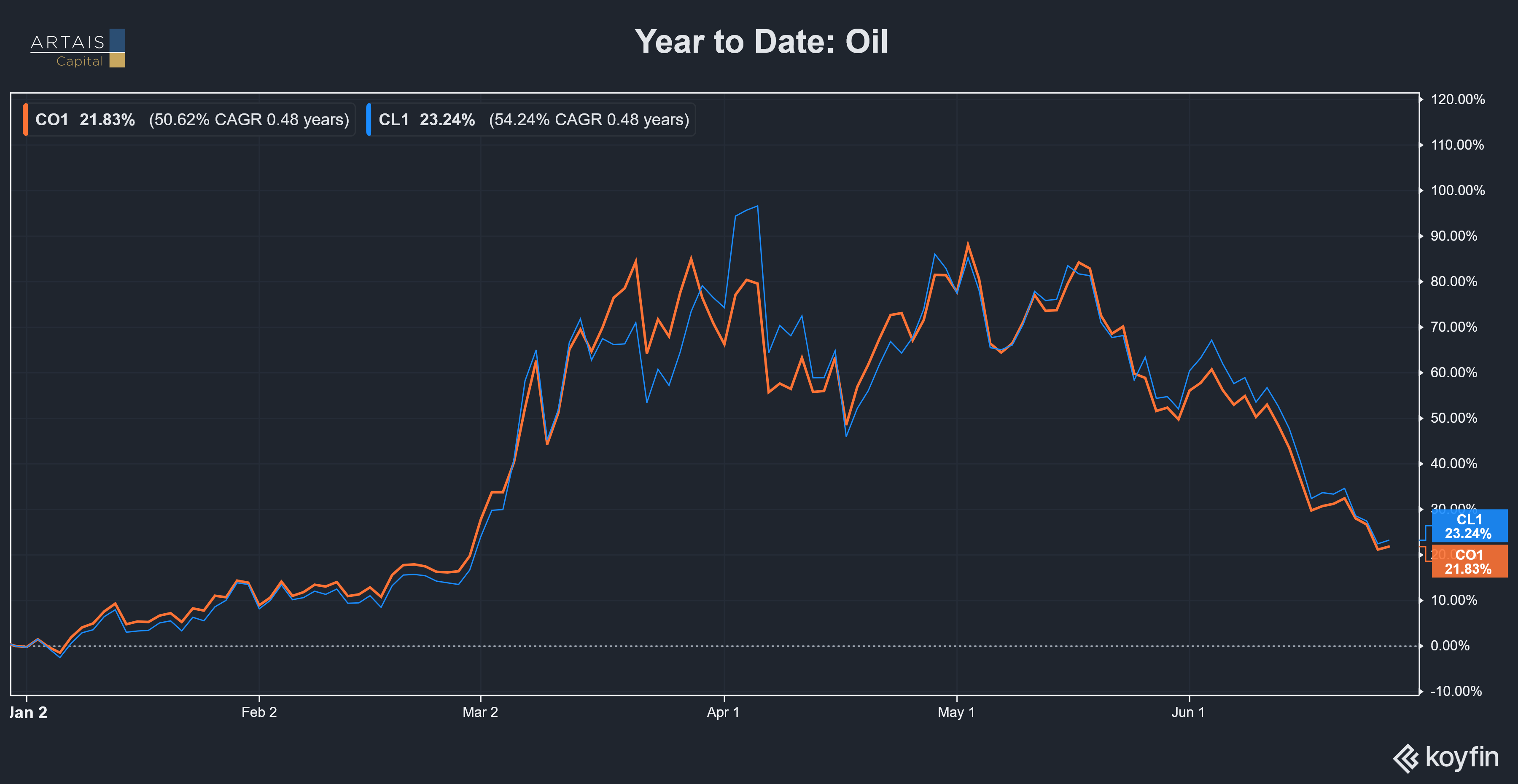

What Actually Happened

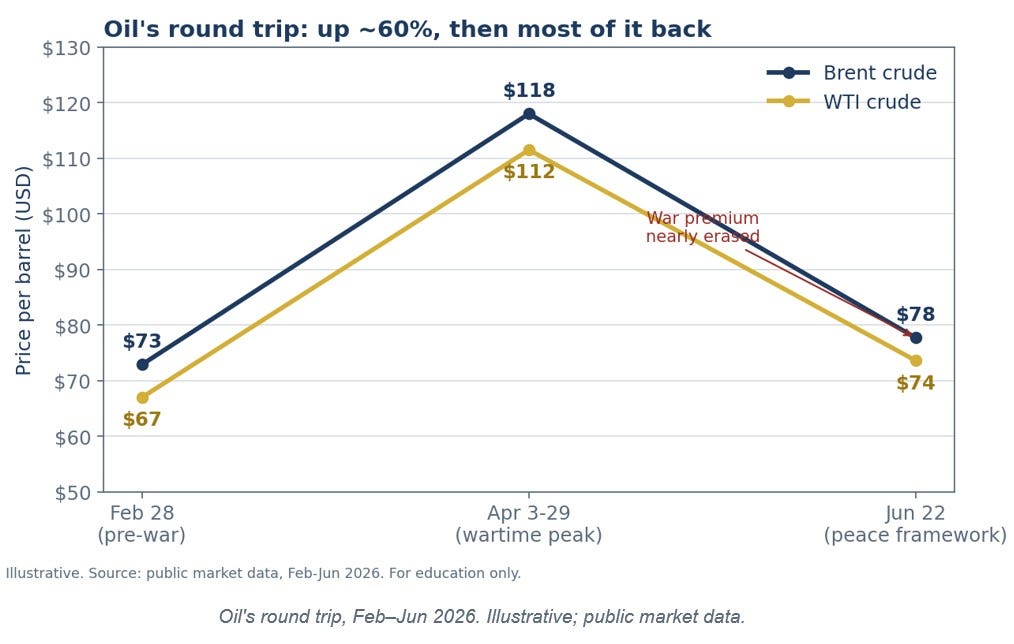

When the U.S. and Israel struck Iran on February 28, Iran moved to choke off Hormuz, and the U.S. blockaded Iranian ports. Oil reacted exactly as the textbook says it should.

West Texas Intermediate went from about $67 a barrel to a peak near $112 in early April. Brent ran from roughly $73 to about $118.

Call it a 60 percent spike in a matter of weeks, driven almost entirely by fear that the supply route would stay closed.

Then, over the past two weeks, the diplomacy turned. A framework emerged, mediated by Pakistan, to end the war, reopen the Strait, and lift the blockade.

The U.S. Treasury issued a 60-day license allowing Iranian crude to trade again. Tanker traffic started inching back through the channel. And the price did the round trip in reverse.

As of this week, Brent sits below $80 and WTI in the low $70s — down more than a third from the wartime peak and only modestly above where they started before the first missile flew.

The market has, in effect, decided the war is over. The fear is being priced out.

BUT — The Strait Has to Actually Open

I want to be careful here, because “peace deal signed” and “oil route fully normalized” are not the same thing, and the gap between them is where investors can get hurt.

The framework is tentative.

Earlier this month, the talks were abruptly postponed for a few days before getting back on track, and the signing is still ahead of us, not behind us.

A 60-day license is a 60-day license — it’s a bridge, not a permanent settlement.

Implementation across a dozen-plus co-signing governments takes time, and the Strait has been a geopolitical pressure valve for fifty years. It can re-tighten.

So the current outlook is a probability, not a certainty.

The most likely path is that the channel reopens and oil stabilizes somewhere in the $65–80 range, with forecasters like JPMorgan already penciling year-end Brent closer to the mid-$60s.

But there is a case to be made that the deal wobbles and oil prices snap part of the way back.

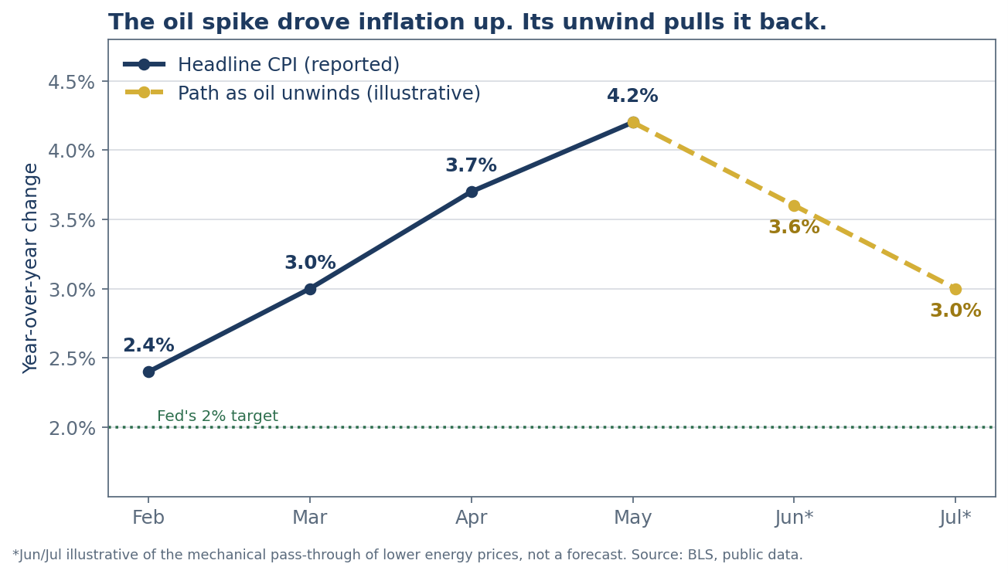

The Inflation Dividend (this is the part that matters most)

Here’s where it gets interesting, and where last quarter’s pain quietly turns into this quarter’s relief.

Energy doesn’t just sit in its own “box” in the inflation data. It leaks into everything — what it costs to fly a plane, truck a pallet, make a plastic bottle, run a farm.

When oil spiked, it dragged the whole inflation index up with it.

Headline CPI, which was running a tame 2.4 percent before the war, jumped to 4.2 percent by May.

That spike is most of why the Fed’s new chair, Kevin Warsh, spent his first weeks talking about nothing but price stability and took rate cuts off the table.

Now run the scenario backward.

Gasoline prices adjust to crude fast, usually within weeks. As the war premium bleeds out of oil, it bleeds out of the inflation data too — first in the June reading, more visibly in July.

This is the single most important takeaway in the whole piece: the same oil move that made inflation look scary is now poised to make it look tame.

A good chunk of that 4.2 percent was always a war tax, not embedded, sticky, wage-driven inflation. War taxes reverse when the war ends.

There are two real consequences:

The first is for households — the energy tax on the family budget is lifting. This puts money back into the pockets of consumers, without anyone getting a raise.

The second is for the Fed. If headline inflation drifts back toward 3 percent and then lower over the summer, the case for a hostile and rate-hiking central bank gets weaker by the month.

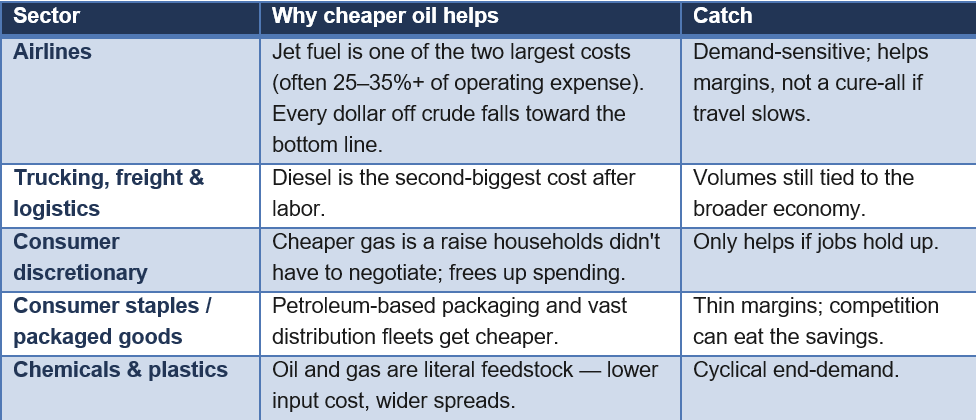

Who Wins When Oil Falls?

When energy gets cheaper, the benefit doesn’t spread evenly. It concentrates in the businesses where fuel is a big, unavoidable line item.

This is the part of the market that was quietly penalized all spring and now gets a tailwind.

Many of these areas were treated as collateral damage during the oil spike.

As the premium unwinds, the same math that hurt them in April starts helping them.

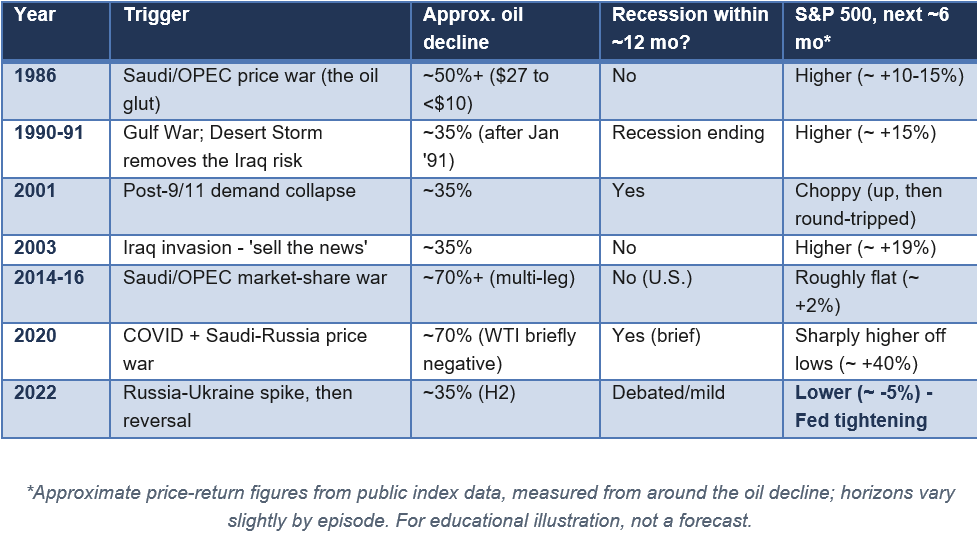

What History Says: The 6 Months After an Oil Scare

This isn’t the first time a geopolitical shock spiked oil and then reversed.

Going back to 1980, the pattern has repeated often enough to be worth studying to see which sector benefited.

Note: The S&P 500’s eleven sectors, as we define them today, didn’t all exist back then.

The official framework (called GICS) only dates to 1999; Real Estate wasn’t split out until 2016, and Communication Services wasn’t reconstituted until 2018.

Here are the major episodes since 1980 in which a geopolitical or supply shock drove oil sharply lower, along with what the broad market did over roughly the following six months.

The most important column in that table isn’t the oil decline. It’s the recession column.

Across roughly seven oil-shock episodes since the mid-1980s, the S&P 500 averaged about a 24 percent gain over the following year, positive in six of seven, with the lone exception being 2008, when oil’s move coincided with a full financial-system breakdown.

What determines the next six to twelve months isn’t the direction oil moved; it’s whether a recession shows up.

And 2022 is the cautionary tale on the other side…

Oil fell hard in the back half of that year, but a Fed in full inflation-fighting mode dragged stocks down anyway.

When the central bank is the dominant force, it can override the oil tailwind entirely — worth remembering with Warsh in the chair today.

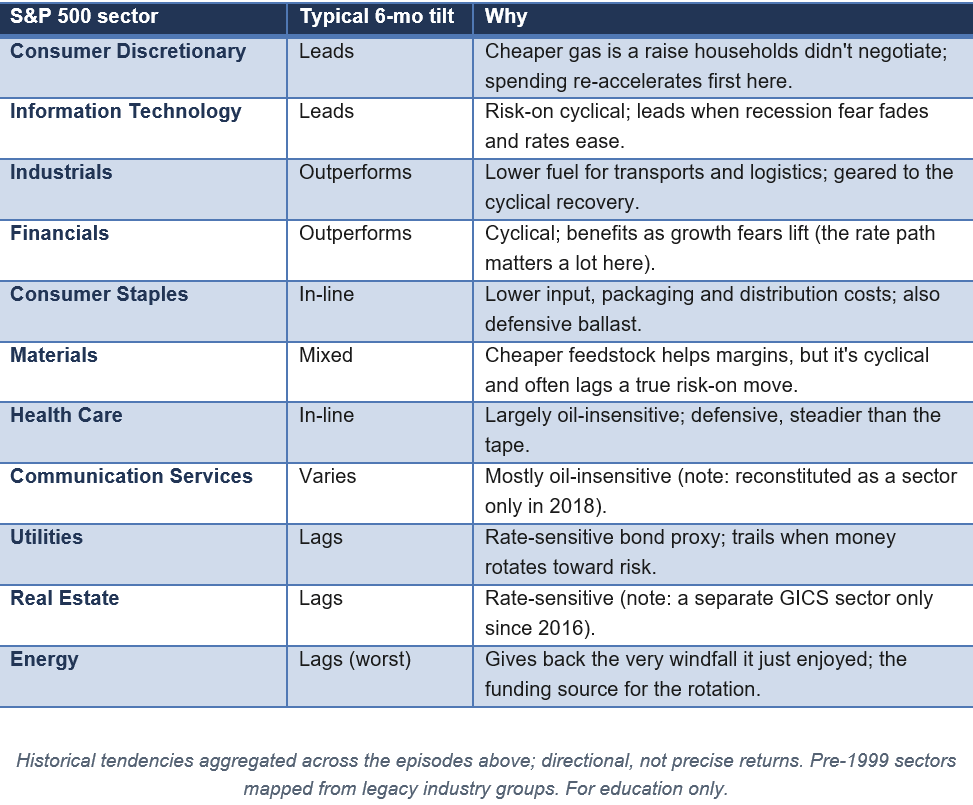

Sector Tilt

When the energy tax on households lifts, the money flows to where people spend it (discretionary), to the firms that move goods more cheaply (industrials and transports), and to the cyclical, risk-on corners that lead once recession fear fades (financials, tech).

Energy is the reliable laggard for the obvious reason. The defensive, rate-sensitive sectors — staples, utilities, real estate — usually trail in the rally but cushion the blow if the optimism proves wrong.

Caution: These are historical tendencies, not promises. Every episode had its own crosscurrents; the sample is small, and “on average” hides a lot of variation.

But AI Growth Needs Energy

When oil dropped, energy stocks dropped with it — many oil and gas names fell 10 to 20 percent in a month, leaving a lot of them below where analysts peg fair value.

The instinct is to read that as “oil is falling, so avoid energy.”

Sometimes that’s right. But it flattens an important distinction. When oil weakens, capital spending slows, the over-levered weak hands get washed out, and the survivors — the companies with clean balance sheets and low breakeven costs — come out the other side with less competition and more pricing discipline.

Selloffs driven by a headline rather than by company fundamentals are exactly where a patient investor goes shopping.

Not every beaten-down energy name; the strong ones with real free cash flow and a reason to exist below $70 oil.

I’m not naming tickers to go buy — that’s not what this article is about. The point is the category logic: a price-of-oil selloff and a quality-of-business problem are two different things, and the market routinely confuses them.

And the real interest in the Energy sector is due to the growth expectations for AI, and the business opportunities it can provide for Energy companies.

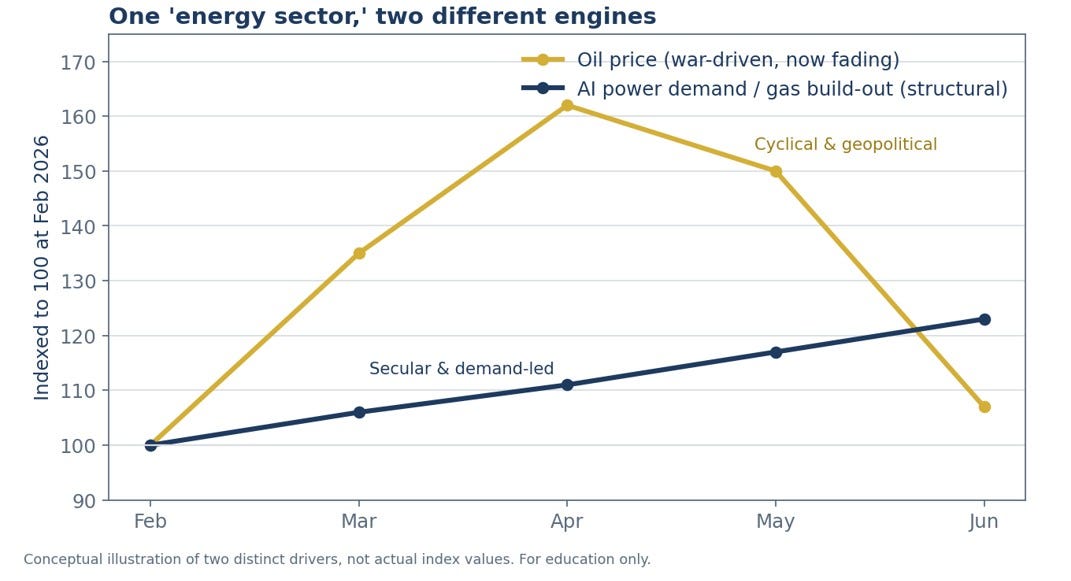

The Energy Sector Isn’t One Story. It’s Two.

Most people hear “energy” and think “oil price.” But the most powerful force in energy right now has almost nothing to do with the price of a barrel.

It’s electricity - specifically, the staggering amount of it that artificial intelligence requires.

Data centers are on track to consume on the order of 1,000+ terawatt-hours of electricity. (If they were a country, that would rank them among the largest power consumers on earth).

And the demand is growing around 15 percent a year, while the rest of the economy’s energy use barely moves.

After two decades of flat U.S. electricity demand, the growth forecast just bent sharply upward.

This is a structural, multi-year shift, and it does not care whether Hormuz is open or closed.

Crucially, a lot of that new demand is being met with natural gas, not oil.

Gas and oil prices have actually been diverging — oil falling on peace, gas firming on AI-driven power demand.

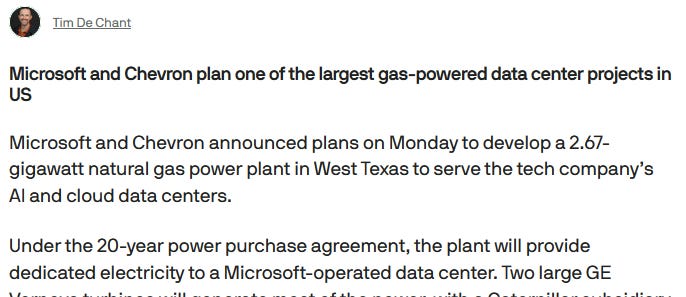

The reason natural gas demand is rising is due to the fact that the public grid can’t connect new mega-projects fast enough. As a result, hyperscalers are building dedicated natural gas plants right next to the data center.

source: TechCrunch

The economics aren’t close. A natural gas plant plugs in for roughly a tenth of the grid-connection cost of solar or offshore wind, and it can be powering servers in about 18 months, versus the multi-year wait for a grid hookup.

That’s why the winners of this growth aren’t only the oil companies — they’re the natural gas producers, the pipeline and “midstream” operators signing multibillion-dollar deals to power data centers directly, and the equipment makers who build the turbines.

One nuance worth flagging: the regulated electric utilities you’d assume are the obvious beneficiaries have actually lagged, because higher interest rates make their bond-like dividends less attractive.

If rates ease as inflation cools (see the section above), the interest in the Ulitlity sector may rise.

Will AI Keep Powering the Growth in Energy?

The case it continues: the demand is contracted, not speculative.

These are signed, multi-year power agreements tied to data centers that are already under construction.

Electricity, unlike a hot stock, is consumed and paid for every single day. And gas is the path of least resistance — cheapest to connect, fastest to build, available around the clock in a way intermittent renewables aren’t yet.

The case it disappoints: AI is getting more energy-efficient at a remarkable clip.

Better chips and leaner models can do more compute per watt, and if efficiency outruns demand, some of these power forecasts will prove too aggressive — the way fiber-optic capacity was massively overbuilt in 2000. (Remember Lucent?)

Build too many gas plants for demand that arrives slower than promised, and you get stranded assets and disappointed shareholders. The grid will also eventually catch up.

Skeptic’s corner

The deal could break. Everything above assumes the framework holds and the Strait stays open. If diplomacy collapses, oil re-spikes, the inflation relief evaporates, and the sector calculus flips. This is the single biggest risk to the whole thesis, and it’s not remote.

Cheaper oil isn’t always good news. Oil falls for two very different reasons: more supply (bullish for everyone else) or less demand (a warning that the economy is slowing). Most of this move is the supply story — Hormuz reopening. But if part of it is demand softening, then “cheaper gas helps the consumer” is cold comfort against a weakening jobs market. Watch which one it is.

The energy stocks may be cheap for a reason. If oil keeps sliding toward the mid-$60s or lower, today’s “oversold” names can get cheaper still, and weaker balance sheets can crack before the survivors re-rate. Oversold is not the same as safe.

Historically, allocators have treated energy as a single positioning call. Reading across 72 manager reports this month, Energy sits at Neutral, with more than half the panel neither adding nor reducing. But your gas-versus-oil distinction is exactly the split that a single sector label obscures. AI-driven natural gas demand doesn't move with the Hormuz headline.

It moves with data center construction timelines and hyperscaler capex decisions. The consensus is Neutral on a sector that is actually running two very different stories at the same time. That is a positioning problem that aggregate data cannot solve.